Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  ECB Signals Possible Interest Rate Move if Inflation Outlook Fails to Improve

ECB Signals Possible Interest Rate Move if Inflation Outlook Fails to Improve  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts

Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts  Bank of Korea Signals Potential Interest Rate Hikes as Inflation Remains Elevated

Bank of Korea Signals Potential Interest Rate Hikes as Inflation Remains Elevated  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing

Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing  South Korea Central Bank Signals Cautious Policy Amid Inflation and Middle East Tensions

South Korea Central Bank Signals Cautious Policy Amid Inflation and Middle East Tensions  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Bank of England Set to Hold Interest Rates as Inflation Risks and Iran War Impact Loom

Bank of England Set to Hold Interest Rates as Inflation Risks and Iran War Impact Loom

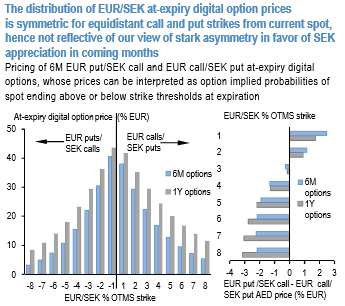

The FX option prices are not priced in the unambiguously positive asymmetry of Swedish Krona spot outcomes. Prices of at-expiry digital (AED) options would be construed as probabilities of spot ending at or beyond strike thresholds at maturity, and are useful for studying the option-implied likelihood of spot outcomes.

One side-effect of the correction in EURUSD has been that PLN and SEK, both of which we like, have fallen further against the dollar than the euro has. That’s not a new pattern and points to heavy positioning, as many people bought ‘euro-alternatives’ rather than the real thing, earlier this year. The upshot is a sizeable bounce in GBPSEK and GBPNOK this month.

The above chart plots the implied distribution of EURSEK over 6-month and 1-year forward windows using EURSEK AED option prices for strikes of varying moneyness.

More than absolute probabilities of up or down moves that can be difficult to assess on a standalone basis, the standout feature of the plot is the lack of any discernible skewness in bullish and bearish outcomes; if anything, the RHS panel shows that strikes beyond ±2% from current market price EUR calls/SEK puts more expensively (i.e. more likely) than comparable % OTMS EUR puts/SEK calls, which militates against the balance of FX risks laid out above and is a textbook instance of disconnect between option market pricing and macro assessment of the spot distribution.

We favor buying zero-cost combinations of long EUR put/SEK call vs. short EUR call/SEK put digitals to position for an eventual normalization of Riksbank policy; JPMorgan’s macro view on SEK has long been tilted in favor of significant krona appreciation, albeit with uncertainty around timing given Riksbank's intransigence in adjusting ultra-loose monetary policy even in the face booming economic growth. The degree to which Swedish monetary policy is way out of step with economic conditions can be gauged.

While the ECB’s hopes of a sustained higher inflation rate have received yet another blow. In September, the inflation rate without the volatile prices for energy, food, alcohol, and tobacco retreated to 1.1%.

Hence, we reckon that the ECB will not be increasing key interest rates so soon.

For instance, off spot ref: 9.6330, 6M 9.30 EUR put/SEK call vs. 9.70 EUR call/SEK put at-expiry digital risk-reversal has a net premium credit of more than 2% EUR. The short strike is above the YTD high, hence reasonable cushion against a backup in spot.