China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation  Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow

BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow  Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform

How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning  Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

The Christmas came early yesterday as CBT refrained from raising interest rates, contrary to consensus expectations. CBT explained its inaction by wanting to wait and see the inflationary effects of the lira’s recent depreciation.

In other words, CBT are adopting the ostrich strategy of sticking their heads in the sand and hoping for the best. This is not an advisable strategy. Inflationary pass through dynamics are especially elevated in Turkey precisely because the central bank implicitly favor weaker exchange rates in the hope of bolstering growth.

Consequently inflation expectations remain elevated and illustrate a high correlation with lira exchange rates. This is to say nothing of external factors. The paradigm shift in long end DM interest rates and the USD implies further upside for USDTRY.

It’s not beyond the realms of possibility to expect a fully blown currency crisis in Turkey in the New Year if CBT’s approach doesn’t change. Markets seem to agree; USDTRY back end volatilities are increasing notably. Put simply, either you deal with a problem or the problem ends up dealing with you.

This central bank’s decision has kept the USDTRY’s long lasting bullish rout. You could this in technical charts that major uptrend has been restrained at 3.5971 levels, swings are going in sideways ever since then.

Technically, the bullish momentum reduced but upswings consistently spiking higher above DMAs, hence, we reckon that despite there is shrink in momentum, the major uptrend has been robust. You could figure out the intensity in weekly charts that signifies the price action, volumes and technical indication by both RSI and moving averages that signal bullish convergence.

So, our strong conviction is that bull trend is likely to prolong in the weeks to come.

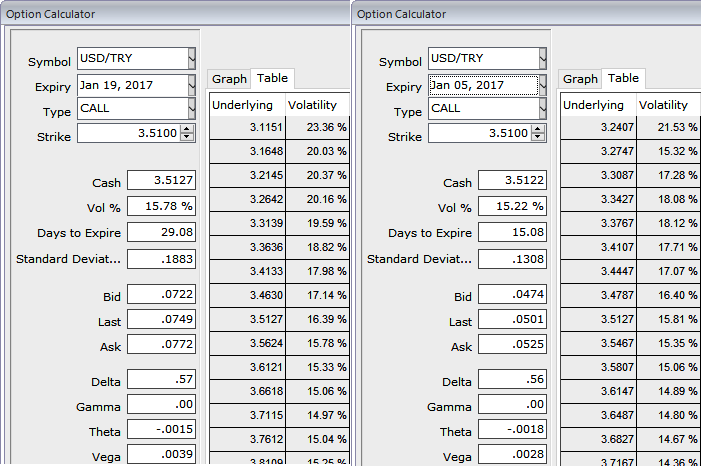

Please be noted that the ATM IVs of 1m and 2w are spiking on higher sides at 15.78% and 15.22% respectively, against a backdrop of a widening current account, ongoing political risks and rising oil prices, we remain firm with bullish bias and hold USDTRY 1x1 call spreads (3.5050, 3.70) which is a debit call spread, at spot ref: 3.5117 levels.

The only positives for lira here, in our view, are extended short speculative lira FX positioning, which likely remains in place even following the short squeeze earlier this week.

Additionally, we understand the government is encouraging state institutions to convert FX holdings into lira. Both of these sources of support are likely to prove limited and can only slow rather than reverse the lira slide, in our view.

Acknowledging the positioning, we continue to hold 1x1 call spreads, however following the government’s package there is now a larger risk of a more aggressive sell-off. Continued non-resident outflows from the local bond market are also likely to drive further TRY weakness.