3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online  Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation

SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

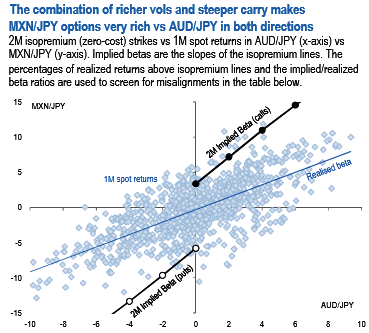

Pick up relative value in conditional spreads, the conditional long/short vanilla spreads provide another avenue to explore when looking to fade vol risk premia. The idea is to structure zero-cost (or even premium negative) spreads of out-of-the-money vanilla options between two well-correlated pairs sharing a common pivot currency.

Opportunities arise when vols and skews in one pair diverge markedly from the other pair. Unsurprisingly, this is currently the case for MXNJPY vs other high beta JPY.

The above chart illustrates as to how the blow up in 2M MXNJPY vols and skews relative to AUDJPY is pushing the lines of isopremium strikes away from the cloud of realized spot returns. According to this picture, MXNJPY calls can be sold to fund AUDJPY calls, and as long as the implicit long AUDMXN stance isn’t upset in a dramatic fashion, the position should pick up positive theta.

Table 2 screens from a large universe of USD, EUR, JPY, GBP and AUD pairs to identify other such opportunities, applying filters on 1) 1yr realised R-Squares between 1M spot returns > 50%, 2) % of spot returns above isopremium line either > 30% or < 70%, and 3) log(Impl/Realised Beta ratio) > 0.25.

We also highlight the combinations that result in implicit cross pair stances that are consistent with our macro bias. The table ranks the combinations according to how far the % above isopremium is from the 50% mid-mark. It suggests that a vol carry efficient way to engineer a long USDCAD position is through a JPY pivot, by buying CADJPY puts funded by selling USDJPY puts.