BOJ Rate Hike Expectations Grow as Board Member Signals Hawkish Stance

BOJ Rate Hike Expectations Grow as Board Member Signals Hawkish Stance  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Bank of Korea Signals Potential Interest Rate Hikes as Inflation Remains Elevated

Bank of Korea Signals Potential Interest Rate Hikes as Inflation Remains Elevated  Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing

Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

Softer vols may prove a momentary soft patch as the Dow Jones broke the symbolic threshold of 20000 last week, bears resume again claw back to 19885 during earlier European session, tripling in nominal value since the lows of 2009, markets seem wrapped up in a spell of euphoria that can only signal radiant optimism on US cyclical upturn and immense credit granted to Trump's emphatic "America First" agenda of protectionism: fiscal easing, infrastructure spending, and deregulation.

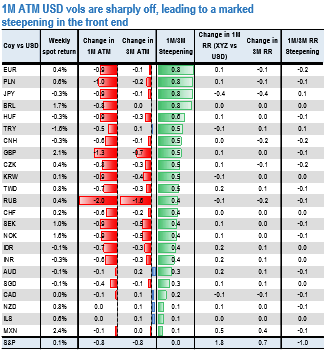

While DXY vols have been easing consistently since US polls results, now in equity markets, a decent start to the Q4 earnings season is further helping vols flirt with all-time lows. At 8.5, 1M S&P vol is just a few decimal points above the abnormally low trough of Jun-Jul 2014. While the price action in FX vols doesn’t suggest the same level of complacency, this softness in front end vols is spilling over to 1M USD vols and sending them sharply lower across the board (refer table).

Fed Chair Janet Yellen has backed a strategy for gradually raising rates, arguing in remarks a day before Trump’s inauguration last week the bank wasn’t behind the curve in containing inflation pressures but nevertheless can’t afford to allow the economy to run too hot. Yellen said wages had risen “only modestly” and manufacturing was operating well below capacity.

As March FOMC and the first round of a particularly disputed French presidential elections keep 3M vols firm, this is leading to a marked vol steepening. Such moves are a hallmark of either capitulation or opportunistic profit taking from investors who started the year with a long vol bias -many of them reluctantly as the position suffered from the frailty of garnering a broad consensus.

Long USD IMM positioning at 1yr highs have certainly played a catalyst role in this capitulation, and the upcoming Chinese New Year period of Asian market closures is likely adding to the mood.

The market vexation with front end USD vols is hardly justified by actual gamma performance, at least if one looks at vol swap returns YTD (refer above chart), and one would be more justified in judging EUR cross vols as expensive to hold (refer above chart). It is not the case that USD gamma is painfully underperforming as of yet, especially when a pair like GBPUSD is able to deliver its largest short squeeze rally since the Brexit vote.

Even USDJPY 1w vols are at the low range of expiries after BoJ’s inaction in the last meeting. Thus the vol softening looks more like temporary setback than a full-fledged vol cleanout, where there remain unresolved issues for global growth (how much growth will Trump's program actually deliver, how does an equity bull run reconcile with a Fed tightening cycle) and the spectrum of a tail-risk sell-off continues to loom over bond markets.