Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations  Denmark Central Bank Intervenes to Support Krone Peg Against Euro

Denmark Central Bank Intervenes to Support Krone Peg Against Euro  AI can be a personal trainer in your pocket – but is it safe?

AI can be a personal trainer in your pocket – but is it safe?

US Treasury yields moved 3-6bp higher over the first half of the week, as domestic producer prices and import prices came in higher than expectations, and the May refunding auctions all tailed amid weakening in end-user demand (refer above nutshell).

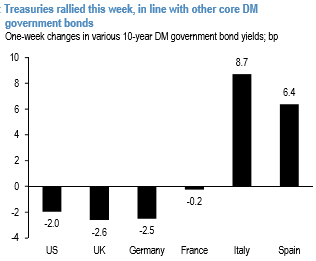

However, this more than fully reversed following Friday’s benign April CPI reading. Since our last publication, front-end and intermediate Treasury yields declined 1-4bp, and the US broadly outperformed other DM government bond markets (refer histogram chart).

But still, with the unemployment rate sitting at its lowest levels of the expansion, matching the 2006 lows, and below the Fed’s year-end and longer-run projections, we continue to expect that the tightness of labor markets will drive the Committee to raise rates by 25bp at the next policy meeting on June 13-14.

Certainly, OIS markets are pricing approximately two thirds odds the Fed will raise rates next month, suggesting limited room for very front-end rates to move higher over the near term, but cyclical dynamics suggest intermediate yields can rise over the next few weeks ahead of the FOMC meeting. The yields have consistently risen ahead of FOMC meetings which are accompanied by an SEP and a press conference.

The third ogive chart shows that over the past two years, 5-year Treasury yields have risen by an average 5bp in the month leading up to long-form FOMC meetings, and this has occurred prior to 7 of the last 8 meetings.

We are bullish on the Ultra 10-year (UXY) contract weighted calendar spread. Wildcard optionality is modest while asset managers are net short. Furthermore, this contract has consistently richened into the first notice date since its inception.

We are bearish on the 10-year note (TY) contract weighted calendar spread. Asset managers and central banks are again net long, whose positions have proven a reliable driver of price action through the roll. Beyond this, the calendar roll has exhibited a strong cyclical tendency to narrow into the first delivery date.