Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails

Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails  JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026

JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026  USA at 250: the Black American struggle for life, liberty and the pursuit of happiness

USA at 250: the Black American struggle for life, liberty and the pursuit of happiness  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  Morgan Stanley Names BAE Systems Top European Defence Stock Despite Lower Price Target

Morgan Stanley Names BAE Systems Top European Defence Stock Despite Lower Price Target

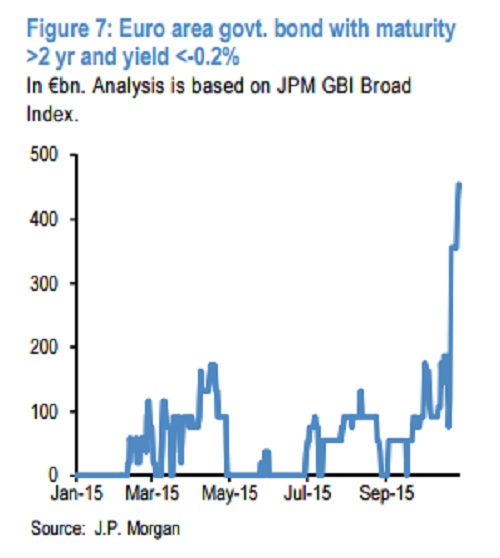

European Central Bank (ECB) president Mario Draghi, in his last policy meeting left the door open to all kinds of adjustment to its super easy monetary policy, ranging from deposit rate cut to tweak in asset purchase program by various parameters or combination of many.

However, market seems to be fixated over at least deposit rate cuts. From the current market pricing a deposit rate cut by European Central Bank as near surety.

Analysis by US investment bank J.P. Morgan showed -

- As of now almost € 454 billion worth of longer duration (2 year-30 year) European bonds are trading below deposit rate of -0.2%, making them not eligible for European Central Bank's (ECB) asset purchase program. The surge in the amount (shown in the chart) has been most prominent since ECB indicated further easing.

- As the calculation goes, almost 11% of the European longer duration (2y-30y) bonds are below deposit rate. For Germany it is almost 30%. Totally 16% or € 1 trillion worth of European bonds are trading in negative.

With such one sided pricing and liquidity it is most likely than not, that European Central Bank (ECB) will reduce deposit rates by 10 basis points further into the negative.

Euro is trading at 1.11 against Dollar.