Trump Questions Housing Bill as He Prioritizes SAVE America Act

Trump Questions Housing Bill as He Prioritizes SAVE America Act  Dollar Slips Ahead of Key U.S. Jobs Data as Fed Rate Outlook, ECB, and Iran Talks Shape Forex Markets

Dollar Slips Ahead of Key U.S. Jobs Data as Fed Rate Outlook, ECB, and Iran Talks Shape Forex Markets  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Asian Currencies Stay Range-Bound as Investors Eye China Data, RBNZ Outlook and U.S.-Iran Ceasefire

Asian Currencies Stay Range-Bound as Investors Eye China Data, RBNZ Outlook and U.S.-Iran Ceasefire  Asian Stocks Slip as US-Iran Ceasefire Hopes Lift Oil, Dollar Strength Persists

Asian Stocks Slip as US-Iran Ceasefire Hopes Lift Oil, Dollar Strength Persists  Gold Prices Drop as Fed Rate Outlook and Iran Tensions Weigh on Market

Gold Prices Drop as Fed Rate Outlook and Iran Tensions Weigh on Market  US Dollar Slips After PCE Inflation Data as Fed Rate Hike Expectations Stay Elevated

US Dollar Slips After PCE Inflation Data as Fed Rate Hike Expectations Stay Elevated  Argentina Economy Shrinks 1.5% in April, Recovery Under Milei Loses Momentum

Argentina Economy Shrinks 1.5% in April, Recovery Under Milei Loses Momentum  FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022

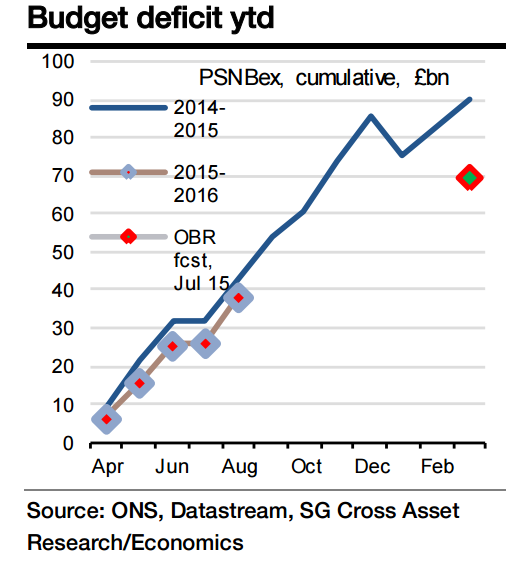

The monthly evolution of the budget deficit is highly erratic. In the first three months of the fiscal year, the PSNBex measure fell by a total of £6bn compared to a year earlier but then in the following two months was £1.6bn worse. So the year-to-date (August) improvement is £4.4bn. However, for the OBR projections for the full year to be met, the improvement would have to have been twice that.

The quality of the data on some of the key inputs is poor until quite late in the year so we should not be surprised at this volatility. Moreover, this also means that we should be cautious in interpreting the year-to-date performance as implying that the full year projection will be missed.

"For September we predict that the deficit will be the same as a year earlier at £11.0bn," notes Societe Generale.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

UK public finances improvement to stall temporarily in September

Monday, October 19, 2015 8:54 PM UTC

Editor's Picks

- Market Data

Most Popular