In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’

State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’  Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  Goldman Sachs Flags 3 Key Risks Ahead of Europe’s Earnings Season

Goldman Sachs Flags 3 Key Risks Ahead of Europe’s Earnings Season  AI can be a personal trainer in your pocket – but is it safe?

AI can be a personal trainer in your pocket – but is it safe?  Trump has made more than $1 billion from crypto in a year. How?

Trump has made more than $1 billion from crypto in a year. How?  Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails

Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails  Vietnam’s population hit the 100 million milestone. Where’s it headed?

Vietnam’s population hit the 100 million milestone. Where’s it headed?

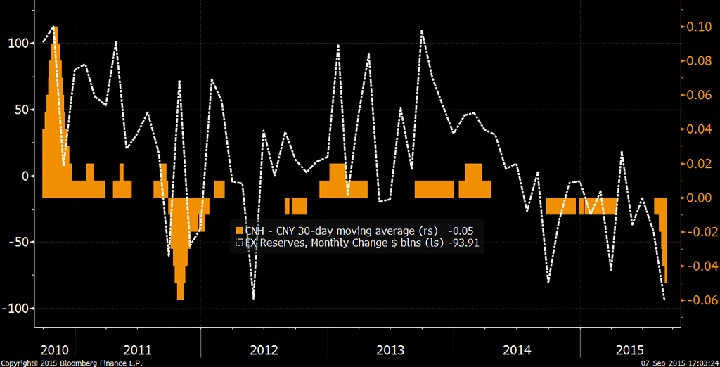

China's gigantic forex reserve, fell by $94 billion in August to 3.56 trillion (approx.), lowest level since 2013.

On August 11th China depreciated onshore Yuan via fix (trading mid-point released by Peoples Bank of China just before trading opens) by 1.9%, biggest devaluation in more than two decade. Beijing continued three days of consecutive devaluation.

Officially PBoC has said this move is a onetime effort, which takes into account FED's interest rate hike policy and the value of fix will now take into account CNH closing as well as changes in major currencies.

What many analysts (including us) argues that it actually was is a defacto peg break. PBoC incurring heavy cost to hold the Yuan/Renminbi around 6.2 against Dollar amid capital outflow, so devaluation was PBoC's effort to release some of the pressure and not to sell Dollar cheap.

Latest report on reserves provide evidence of such.

In spite of the devaluation, (according to us, due to the devaluation) PBoC is still experiencing heavy capital outflow pressure thanks to unwinding in short term position (Yuan isn't one way trade). In spite of its positive trade balance and FDI flows, sharp fall in FX reserves suggest heavy intervention by PBoC and capital flight. It could be somewhere between $110-120 billion.

Expect further capital flight, more the reserves bleed and depreciation, greater will be the pressure.

If not convinced, have a look at the widening spread between onshore and offshore Renminbi. Offshore Yuan is now trading at a considerable discount suggesting further capital flight continuation in September. While onshore Yuan is trading at 6.36 per Dollar, offshore is trading at 6.48 per Dollar.

Have a look at history, chart courtesy Bloomberg.