State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’

State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’  Bernstein Names IAG, Ryanair as Top European Airline Stocks Ahead of Earnings

Bernstein Names IAG, Ryanair as Top European Airline Stocks Ahead of Earnings  Bank of America Upgrades T-Mobile to Buy, Says LEO Satellite Fears Are Overdone

Bank of America Upgrades T-Mobile to Buy, Says LEO Satellite Fears Are Overdone  Goldman Sachs Raises USD/JPY Forecast, Sees Yen Weakness Persist Through 2027

Goldman Sachs Raises USD/JPY Forecast, Sees Yen Weakness Persist Through 2027  Goldman AM Sees Strong Buyout Opportunities in Japan, South Korea and Australia

Goldman AM Sees Strong Buyout Opportunities in Japan, South Korea and Australia  Vietnam’s population hit the 100 million milestone. Where’s it headed?

Vietnam’s population hit the 100 million milestone. Where’s it headed?  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  Citi Raises TSMC Price Target as AI Chip Demand Strengthens Growth Outlook

Citi Raises TSMC Price Target as AI Chip Demand Strengthens Growth Outlook  Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails

Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails

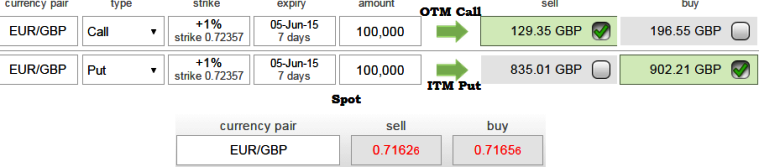

Here we assumed the portfolio contains the same expiration for calculation purpose (it actually has to be near month on call shorting & far month on put) with two different currency derivatives instruments of same underlying currency then they must have the same present value.

Else, arbitrager can go long on the undervalued portfolio and short the overvalued portfolio to make a risk free profit on expiration day.

Hence, taking into account the need to calculate the present value of the cash component using a suitable risk-free interest rate, we have calculated and illustrated the Put call parity of EUR/GBP collar:

C = S + p - Xe-r (T- t)

= 0.7162 + 902.21 - Euler (0.7235*2.71828) - 0.02*(7)

= -901.1

P = c - S + Xe-r (T- t)

= 129.35 - 0.7162 + Euler (0.7235*2.71828) - 0.02*(7)

= 126.8071

Where,

S = Current Exchange Rate

X = Exercise price (strike) of option

C = Call Value

P = Put price

e = Euler's constant - approximately 2.71828 (exponential function on a financial calculator)

r = continuously compounded risk free interest rate = assumed at 2%

T-t = term to expiration measured in years

T = Expiration date

t = Current value date

Note: Before jumping into a conclusion of above calculations, one has to be mindful of how the supply and demand impacts option prices and how all option values (at all the available strikes and expirations) on the same underlying security are related.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Put call parity of EUR/GBP collar

Friday, May 29, 2015 9:09 AM UTC

Editor's Picks

- Market Data

Most Popular