Smartphones are helping filmmakers tell the stories the movie industry overlooks

Smartphones are helping filmmakers tell the stories the movie industry overlooks  Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit

Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit  USA at 250: the Black American struggle for life, liberty and the pursuit of happiness

USA at 250: the Black American struggle for life, liberty and the pursuit of happiness  Trump has made more than $1 billion from crypto in a year. How?

Trump has made more than $1 billion from crypto in a year. How?  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  Vietnam’s population hit the 100 million milestone. Where’s it headed?

Vietnam’s population hit the 100 million milestone. Where’s it headed?  Citi Raises TSMC Price Target as AI Chip Demand Strengthens Growth Outlook

Citi Raises TSMC Price Target as AI Chip Demand Strengthens Growth Outlook  State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’

State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’  Goldman AM Sees Strong Buyout Opportunities in Japan, South Korea and Australia

Goldman AM Sees Strong Buyout Opportunities in Japan, South Korea and Australia  Goldman Sachs Raises USD/JPY Forecast, Sees Yen Weakness Persist Through 2027

Goldman Sachs Raises USD/JPY Forecast, Sees Yen Weakness Persist Through 2027

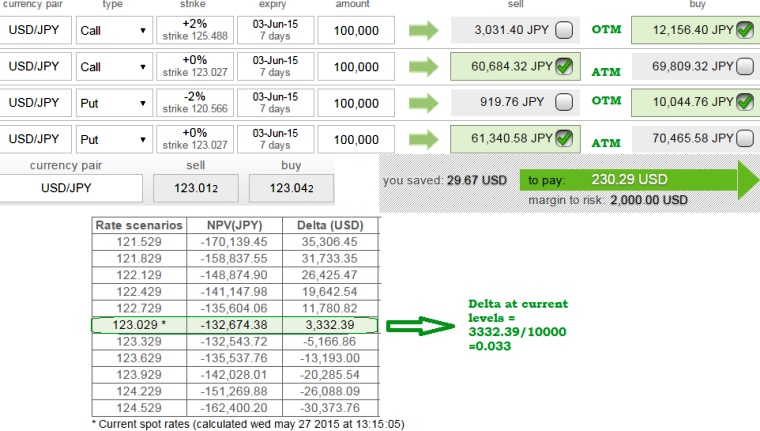

The rate of change option portfolio to a relative change in the spot market price of the underlying currency is shown as below:

For instance in our earlier post we had advocated iron butterfly, where ATM Call & Put were sold and simultaneously OTM Call & Put were bought on this pair.

Let's just revisit on this portfolio that was built earlier:

The OTM call has now at current a delta of 0.10 and the price of the underlying goes up by $0.0004, the value of the call could be expected to go up by approximately $0.0002.

While ATM call, delta approaches 0.50.

The OTM put has now at current levels a delta of 0.89, so any smaller change in the market price of the underlying will produce very little change in the value of the put.

If a put has a delta of 0.5 and the price of the underlying goes down by $0.0002, the value of the put could be expected to go up by approximately $0.0001.

As a whole, the strategy has been nearing delta at zero (accurately at 0.03) as shown in the figure.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Portfolio analysis on Iron butterfly USD/JPY

Wednesday, May 27, 2015 8:05 AM UTC

Editor's Picks

- Market Data

Most Popular