New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery  JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026

JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026  USA at 250: the Black American struggle for life, liberty and the pursuit of happiness

USA at 250: the Black American struggle for life, liberty and the pursuit of happiness  BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks  RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists

RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists  Goldman Sachs Flags 3 Key Risks Ahead of Europe’s Earnings Season

Goldman Sachs Flags 3 Key Risks Ahead of Europe’s Earnings Season  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

SNB convenes on 17 September to announce the quarterly monetary policy assessment and is widely expected to keep the key policy rates unchanged at -0.75%. Although the international environment has become more uncertain, Switzerland continues to show some positive signals. The outlook for Switzerland's economy has turned broadly positive for the first time in a year, with businesses beginning to absorb the shock of January's effective revaluation of the franc.

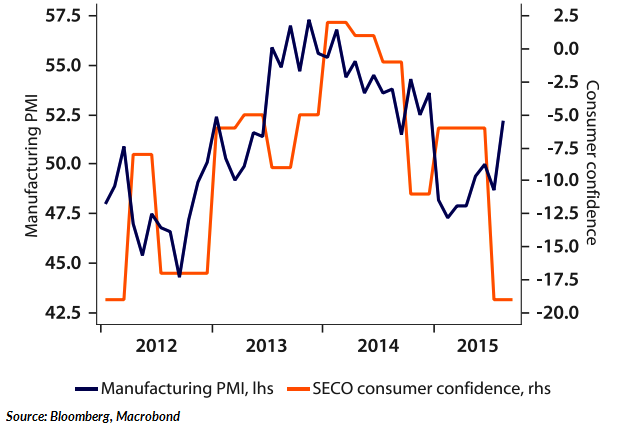

Recent soft economic data have been mixed. Consumer confidence fell sharply to -19 in August, but the purchasing managers index increased and is currently above the 'neutral' 50-mark. The economy avoided a technical recession in Q2, with a much better than expected growth of 0.2% q/q (-0.1% expected) after a contraction in Q1. Data shows that companies in Switzerland's export-dependent economy had shown themselves better able to adjust to the strong franc than expected, while consumption has also proven very stable.

The main worry for the SNB remains inflation, which is expected to have remained in negative territory in August (consensus: -1.4%). President Jordan said that Swiss deflationary pressures have a different origin than those of countries such as Japan. Indeed, Switzerland is still feeling the pain from the sharp currency appreciation in previous years. Sharp fall in oil prices are also seen as the main reason behind these sub-zero inflation readings.

That said, CHF's correlation with volatility indices (for example the VDAX) has become positive, which means that news bouts of volatility result in a weakening of the Swiss franc. The Swiss franc is no longer the first choice as a safe haven for investors and has weakened vis-à-vis its major trading partners. Also the oil price increase of around 20% in recent days can be seen as a positive surprise for inflation.

In a recent interview, SNB president Thomas Jordan said that he sees no reason for a change in policy, but that the SNB stands ready to intervene. This means that the rate on sight deposits will probably not be adjusted downwards and will remain at -0.75%, when the SNB convenes on 17 September.

The central bank will try to calm the markets, if necessary, via verbal intervention. For example, by repeating its comments that the franc is markedly overvalued and that the Swiss National Bank stands ready to intervene if necessary. But, as the Swiss franc is currently weakening vis-à-vis the euro, there is no immediate need for intervention.

"In the absence of significant EUR weakness we think the SNB will accept things as they are given its toolbox constraints. Thus we expect the SNB to keep the key policy rates unchanged at -0.75% in September. Pricing is for a gradual normalisation of SNB rates (and no more cuts) as late as 2017; we see this as largely fair." notes Danske Bank in a research note to its clients.

USD/CHF range bound, plays 0.9735/93 on the day. EUR/CHF cross off 1.0971 highs (1.0983 Tues top), trades at 1.0935 at 1126 GMT

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

No immediate need for SNB to intervene

Thursday, September 10, 2015 11:40 AM UTC

Editor's Picks

- Market Data

Most Popular