Gold Price Holds Above $4,000 as Fed Rate Hike Expectations and U.S. Jobs Data Weigh on Market

Gold Price Holds Above $4,000 as Fed Rate Hike Expectations and U.S. Jobs Data Weigh on Market  Wall Street Ends Mixed as Weak Jobs Data Lowers Fed Rate Hike Bets, Chip Stocks Tumble

Wall Street Ends Mixed as Weak Jobs Data Lowers Fed Rate Hike Bets, Chip Stocks Tumble  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027  Smartphones are helping filmmakers tell the stories the movie industry overlooks

Smartphones are helping filmmakers tell the stories the movie industry overlooks  USA at 250: the Black American struggle for life, liberty and the pursuit of happiness

USA at 250: the Black American struggle for life, liberty and the pursuit of happiness  JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026

JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026  Gold Price Today: Bullion Heads for First Weekly Gain as Weak U.S. Jobs Data Eases Rate Hike Fears

Gold Price Today: Bullion Heads for First Weekly Gain as Weak U.S. Jobs Data Eases Rate Hike Fears  China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  US Stock Futures Hold Steady Ahead of June Jobs Report as Fed Rate Outlook Remains in Focus

US Stock Futures Hold Steady Ahead of June Jobs Report as Fed Rate Outlook Remains in Focus  New Zealand Consumer Confidence Rises in June as Inflation Expectations Ease

New Zealand Consumer Confidence Rises in June as Inflation Expectations Ease  Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey

Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey  RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

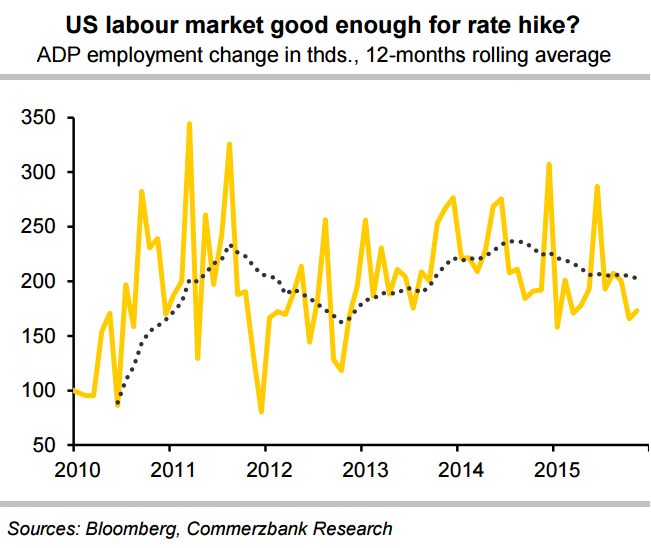

The FOMC minutes of the June meeting provide little insight as the meeting took place before the EU referendum. Most participants noted that the upcoming British referendum on membership in the European Union could generate financial market turbulence that could adversely domestic economic performance. In addition to worries about Britain and the EU, some officials expressed concerns about uncertainties surrounding China's future moves in managing its currency and the impact of relatively high levels of debt on the Chinese economy.

FOMC meeting minutes also underscored questions about prolonged softness in business investment spending. Fed officials attributed much of the weakness to the big plunge in oil prices, which had triggered cutbacks at energy companies. “Some” on the Fed policy committee thought that labour market conditions and inflation were close to the Fed’s goals. But a couple of members said they would need “sufficient evidence to increase their confidence that economic growth was strong enough to withstand a possible downward shock to demand and that inflation was moving closer to 2% on a sustained basis.”

“The July FOMC meeting is certainly off the table. September is in play I suppose, but only if everything breaks perfectly. November is out of the question, in my view, given that it falls less than a week before the presidential election. That leaves December, which is currently my expectation for the next Fed move,” said Stephen Stanley, chief economist at Amherst Pierpont Securities, summing up the thoughts of many Fed watchers.

As economic data improves, which has already begun to materialize with growth in GDP in Q2 expected around 3 percent q/q annual rate, the Fed should become confident enough to raise rates sometimes in the second half of 2016. US ISM non-manufacturing index rose 3.3p to 56.5 in June, beating consensus at 53.3. The data was another strong US indicator, pointing towards a pick-up in growth in Q2. However, the trade deficit widened more than expected by $3.8bn to $41.1bn in May and still a drag on GDP growth.

However, financial market turmoil post-UK vote in favour of Brexit and the uncertainty around European banks, indicate that the next rate hike will come later rather than sooner. The Fed's next meeting is scheduled for 27th July. If Friday's US labour market report disappoints once again that would likely be the end of rate hikes this year. Many analysts think even a good jobs report won't be enough to convince policymakers to raise rates, especially in light of the uncertainty triggered by the Brexit vote. Some analysts think the Fed could hold off raising rates until September or possibly even wait until its last meeting of the year in December.

"We expect the Fed to hike rates by 25bp in December and an additional 25bp in June next year," said DNB Bank in a report.

US dollar index subdued on the day, trades around 96.06 levels at 11 GMT. USD/JPY was at 101.11, while EUR/USD at 1.1078.