ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns  China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026

JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026  Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  Buy the Dip: Gold Holds Strong at $3980, Targets $4150

Buy the Dip: Gold Holds Strong at $3980, Targets $4150  Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit

Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

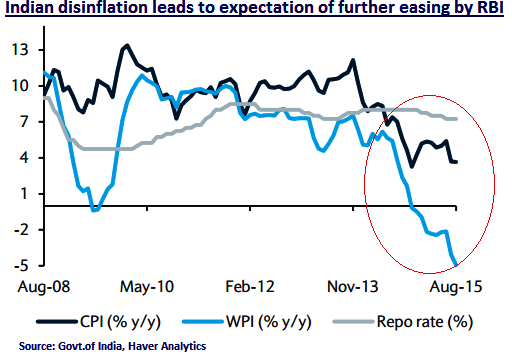

Strong disinflation opens room for further RBI easing, the disinflation in India has been strong and broad-based since H2 2014, reflecting markedly better food price management, sustained idle industrial capacity, lower commodity prices and a largely stable INR.

We expect retail inflation (CPI) to average 5% during FY 15-16, considerably lower than the central bank's early 2016 target of 6% and the long-term (15- year) average of 7.3%.

Disinflation has been even stronger at the wholesale price (WPI) level, which has contracted on y/y basis in every month since November 2014 and is currently near a four-decade low (August 2015: -5.0% y/y).

The renewed weakness in commodity prices in Q3 15 should help keep inflation 'lower for longer'. Despite stronger GDP prints under the 'new' series, we see little sign of demand-driven inflation.

Such rapid disinflation allowed the Reserve Bank of India (RBI) to cut the repo rate by 75 bps during H1 15. We look ahead to the central bank to cut the repo rate another 25 bps in H2-15, likely in its policy meeting scheduled for tomorrow.

What are market participants expecting from tomorrow's policy?

According to Bloomberg Survey of 49 analysts, 41 expect a repo rate cut and 8 expect no change in the RBI's stance on the interest rate. Our expectation is also of a 25 basis point cut in the benchmark repo rate. SLR and CRR are expected to remain unchanged.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Indian disinflation leads pressures on RBI easing

Monday, September 28, 2015 12:46 PM UTC

Editor's Picks

- Market Data

Most Popular