Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit

Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit  Bernstein Names IAG, Ryanair as Top European Airline Stocks Ahead of Earnings

Bernstein Names IAG, Ryanair as Top European Airline Stocks Ahead of Earnings  Gold Pulls Back After Hitting $4,180 as Geopolitical Risk Sends Crude Higher

Gold Pulls Back After Hitting $4,180 as Geopolitical Risk Sends Crude Higher  State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’

State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’  Smartphones are helping filmmakers tell the stories the movie industry overlooks

Smartphones are helping filmmakers tell the stories the movie industry overlooks  Buy the Dip: Gold Holds Strong at $3980, Targets $4150

Buy the Dip: Gold Holds Strong at $3980, Targets $4150  Bank of America Upgrades T-Mobile to Buy, Says LEO Satellite Fears Are Overdone

Bank of America Upgrades T-Mobile to Buy, Says LEO Satellite Fears Are Overdone  Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  Trump has made more than $1 billion from crypto in a year. How?

Trump has made more than $1 billion from crypto in a year. How?  Goldman Sachs Raises USD/JPY Forecast, Sees Yen Weakness Persist Through 2027

Goldman Sachs Raises USD/JPY Forecast, Sees Yen Weakness Persist Through 2027  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

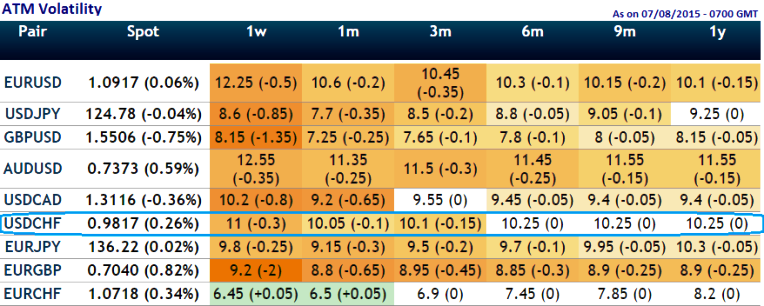

We've been formulating a lot of call spreads on highly volatile currency pairs (USDCHF is the one among the pool, the pair ranks under top three highest among major pairs to perceive volatility of ATM contracts, ATM contracts currently trending at 11% vols) and have been drawing up some customized strategies by using P&L tools and techniques to look at the option Greeks.

While doing so it seems like the OTC option of this pairs have tons of Gamma. It might be puzzling because on one hand it seems some of these options are highly volatile than any other Euro American currency pairs except EUR/USD but a tiny shift in the underlying exchange rate would cause instant disaster. This can be arrested by devoting little time on ascertaining an accurate gamma.

We've constructed call spread by considering gamma closer to zero would neutralize the implied volatility impact on option price and this position remains quite firm to achieve our hedging objectives, because we know gamma represents the change in delta, we have healthier delta at 0.46 at combined position.

This results in desired hedging objective irrespective implied volatility disruptions as we've OTM shorts on side and prevailing bull run will be taken by In-The-Money calls.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirepPro: USD/CHF to perceive HY vols; optimize volatility through gamma spreads

Friday, August 7, 2015 9:46 AM UTC

Editor's Picks

- Market Data

Most Popular