US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

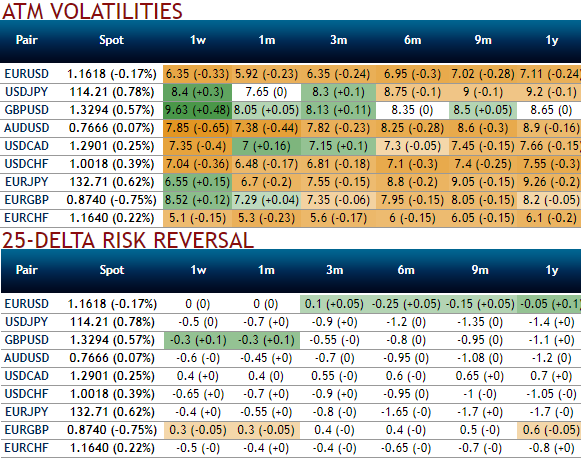

Shift policy dynamics leads euro vols market downside, shrinking IVs, skews and neutral risk reversals lure cheap bearish hedging:

Developments over the past week motivate two changes to our trade recommendations. First, we scale back our EUR longs since with the ECB meeting now behind us and modestly more dovish than expectations, a monetary policy catalyst for euro strengthening will be lacking in the coming weeks.

Before proceeding further, let’s glance through above nutshell evidencing IVs, IV skews and risk reversals of short-tenured ATM contracts of EURUSD. IVs have been shrinking away, these are the least among G7 FX pool, while risk reversals have been neutral. Positively skewed IVs are suggesting the neutral.

Euro downside volatility remains cheap Euro vol market could be more nervous. The vol sell-off can be attributed, at the very least, to the options market unwinding long gamma positions that were built ahead of the ECB meeting. But tactical positioning cannot fully justify such a sell-off because:

1) The fast euro move generated substantial realized volatility, and

2) One could expect the options market to be quite nervous with the spot testing its important horizontal support just above 1.16 (the upper bound of the 2015-2017 range).

No premium (yet) in sub 3m euro puts. Although the options market is now certainly much less confident that we can have imminent topside volatility (as reflected by the softest RR), market pricing is not switching towards substantial bearish risks.

Despite the euro fall, the RR did not return to negative territory and, noticeably, the implied volatility preserved its positive correlation with the FX rate by moving lower alongside it. (Only the 6m RR is priced more negatively because this tenor includes the Italian election expected in early 2018).

All in all, this is a frail equilibrium, and recent dynamics mean short-dated OTM euro puts are still a cheap hedge.

The expectation is for a second ECB policy pivot to be delivered in 2018 which should eventually drive sizable euro strength once again, but gains from this driver will be limited in the near term. In the interim, EURUSD will be more susceptible to US-specific factors which have more dollar bullish as noted earlier, as well as intermittent political risk in the Euro area.