Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

The euro area corporates are in a good position to expand, the corporates in this geography have become net savers and low-interest costs, lower dividend payouts, lower CapEx explains the shift.

Corporates’ capacity to accelerate CapEx looks good.

A couple of months ago, we still expected the Euro area to grow at only a modestly above-trend pace this year. However, business and consumer sentiment have improved sharply, with the composite PMI signaling 3% growth in March. This prompted us to raise our 2017 growth forecast to 2.2% Q4.

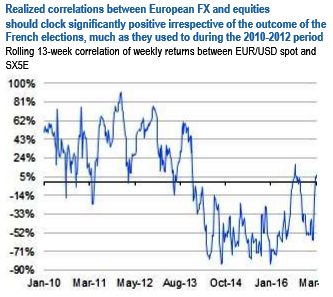

European FX vs. equity implied correlations currently trade in the 0 -20% range in 6M –1Y expiries, which might be fair relative to current realized correlations but ought to reprice higher in coming months if a concerted European asset rally reverts corrs back to average levels of the 2010-2012 period (refer above chart).

Investors have already started to take advantage of this dislocation and forced short-dated (<3M) EURUSD vs. SX5E correlations up to +25%, but there is still room for the move to play out in longer tenors.

EURUSD > 2% OTMS, SX5E > 5% OTMS: dual digitals costs 14.5% EUR indic. in 3M tenors (indiv. digis 43% and 26% respectively) and 18.5% EUR indic. in 1Y (indiv. digis 58% and 37% respectively).