SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

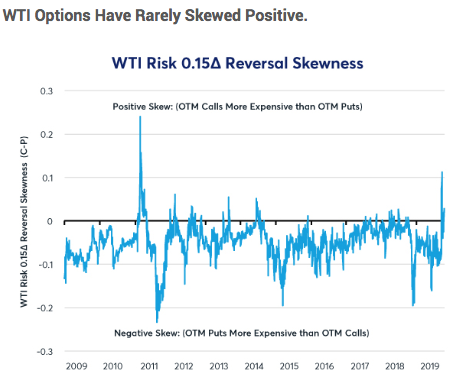

The prices of WTI and other crude oil product are back to the levels where they were when the drone attacks on Saudi oil infrastructure took place a month ago, the prices have now returned to their pre-attack levels (i.e. around $54 a barrel). Huge turbulence was seen in this one-month.

Please be noted that the implied volatility on at-the-money WTI, gasoline and Ultra Low Sulfur Diesel (ULSD) options has also similarly retreated.

However, options skew is well off its highs, remains very different now than before the attacks on the world’s top oil exporter.

Usually, the WTI and oil products skew is negative, meaning out-of-the-money (OTM) puts are more expensive than OTM calls. After the attacks, that skewness flipped: OTM calls became more expensive than OTM puts. Since then, they have gone back in the other direction but remain much less negatively skewed than is typically the case (refer above chart).

Whether WTI and product prices decline this time, as the past relationship between options skews and subsequent movements in prices suggests is more likely than not, depends, of course, on how both fundamental and geopolitical factors play out. If inventories fall sharply, a possibility given that as much as half of Saudi oil output was offline for two or three weeks, that could boost oil prices.

Likewise, any strengthening of global demand or a supply shock of any sort could send prices much higher. Indeed, the options markets is more concerned than usual that such upside could happen.

That said, options skewness has proven to be somewhat of a contrary indicator of near-term price direction over the past decade. It’s often been that when oil traders were most worried about future price declines, prices, in fact, rebounded and when they were most concerned about upside risk, prices have the greatest propensity to fall.

Overall, one month after the Saudi oil infrastructure attacks, prices and ATM volatility are back to normal. Options skews, however, are much less negatively skewed than normal. Courtesy: CME sources