Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Indonesia Passes New Central Bank Law, Raising Investor Concerns Over Policy Independence

Indonesia Passes New Central Bank Law, Raising Investor Concerns Over Policy Independence  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns

Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns  Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027

Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027

Mexican Peso has been edgy on the lingering expectations from analysts for Banxico to hike today and again once before the end of the year, and a 50bp rate increase next week seems more likely than waiting until December.

While waiting for the policy reaction, we note that the uncertainty pending on US trade policies, exacerbated by tighter global financial conditions suggests the MXN is not cheap at current levels.

True, short-term valuation models, which rely on historical co-variances of USDMXN and coincident risk indicators, suggest MXN 2.5-3.0% cheap. Yet, we believe that premium is not enough in case the newly elected US administration decides to pull the trigger on severe protectionist measures (i.e. leaving NAFTA).

Why should the Mexican central bank hike rates today having not raised rates at the press conference called at short notice last week? After all, the peso collapsed notably further. However, the change in market expectations as regards US central bank policy constitutes a new negative factor for the peso that arose this week. Against this background the market has taken the view that the Mexican central bank will have to act to prevent the peso from collapsing.

Most notably, after the recent USD rally caused by Donald Trump’s election victory and based on rising inflation and interest rate expectations continued, the new phase of dollar rallies is still on the cards as the Fed’s Christmas easing is nearing little early.

As a result of the already restrictive monetary policy measures over the course of the year and the expected change of direction in US policy the outlook for the Mexican economy is subdued. Against this background, it would probably be advisable to leave rates unchanged. However, it would probably turn out to be an even worse decision to disappoint the market as it is already nervous due to high uncertainty. By doing that Banxico would risk a further collapse of the peso which could mean that it may have to raise interest rates even further to calm the market.

Short Term Hedging Perspectives:

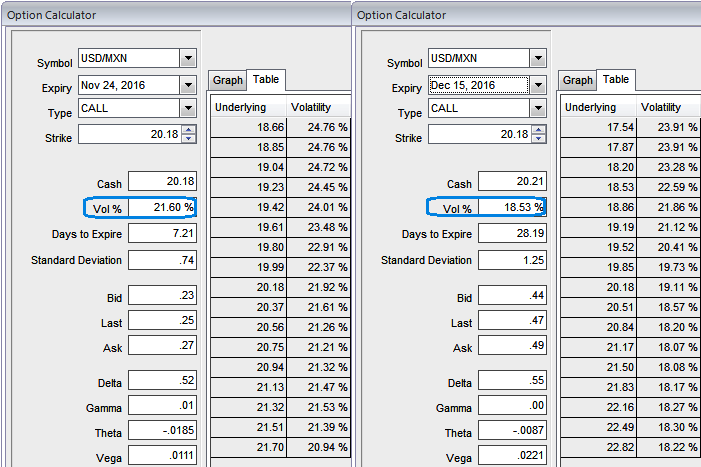

1w ATM IVs are spiking frantically above 21.6% which is quite conducive for option holders when underlying spot keeps plummeting in next 1weeks’ time; this is quite evident in payoff structure during various underlying rate scenarios.

So, as shown in the diagram, this is the option strategy in which the Mexican foreign traders who have their dollar receivable exposures are suggested to buy an at the money put option of 1m tenors while simultaneously buying an equivalent notional amount of the underlying spot FX.

Since purchasing a protective put gives you the right to sell underlying pair at the predetermined strike price, there wouldn’t be any potential threat for this exposure regardless of underlying spot rates.

The strategy is typically employed when the foreign trader is having exposure on the dollar receipts, and he doesn’t want to take any FX risks, but wary of uncertainties in this span of one month.