Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

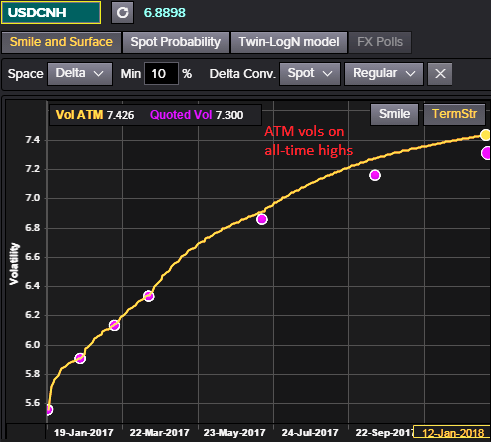

The funding cost of CNH dropped significantly this week, with the HIBOR overnight rates easing to below 3% this morning. In the meantime, the CNY-CNH spread has narrowed significantly. In our view, this is due to the arbitrage flows as corporates took advantage of the wide CNY-CNH spread. In addition, the short CNH positions could start to pick up again with a lower carry cost. Bottom line: the pressure on CNY exchange rates persists, and the market intervention won’t change the market expectations at all.

The biggest talking point of the New Year is the shellacking that China bears have received on consensus long USDCNY positions, engineered via the by-now familiar tool of raising FX implied yields to punitive levels. As you could observe from the diagram showing ATM and implied vols have collapsed and risk-reversals are also likely to collapse alongside the liquidation of USD longs, a chasm has now opened up between implied yields in CNH forwards and option prices that is testing historical extremes along a number of dimensions:

Carry/vol in ATMF USD puts/CNH calls and ATMF – ATMS USD put/CNH call spreads is at multi-year highs. However, a strong dollar through 1H remains the baseline despite the rinse in CNH and related short Asian FX positions this week, so this carry/vol extreme is tricky to monetize unless one subscribes to a contrarian notion of stable or lower USDRMB spot from current levels.

This isn’t out of the question if the bullish dollar thesis comes apart in coming months, but is low odds otherwise since CNY should weaken vs. USD alongside partner currencies in a basket framework that remains the fulcrum of Chinese FX policy (as signaled via an expansion of the CFETS basket in late December). It is possible for USDCNH spot to fall short of current FX forwards by the end of the year despite RMB weakness (1y CNH forward @ 7.17 vs. our Dec’17 target @ 7.10), but the ride along the way is likely to prove bumpy and terminal returns unexciting.