RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists

RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027  ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027

Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027  Denmark Central Bank Intervenes to Support Krone Peg Against Euro

Denmark Central Bank Intervenes to Support Krone Peg Against Euro  USA at 250: the Black American struggle for life, liberty and the pursuit of happiness

USA at 250: the Black American struggle for life, liberty and the pursuit of happiness  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey

Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey  Smartphones are helping filmmakers tell the stories the movie industry overlooks

Smartphones are helping filmmakers tell the stories the movie industry overlooks  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

The key driving force of loonie remains the relative priced pace of policy normalization. The conjecture behind a partial retracement higher in USDCAD is the expectation that relative monetary policy pricing will converge somewhat in the coming quarters. Post the June/July repricing, BoC is now priced to hike 67bps in two years, compared to the 32bp priced for the Fed, which in other words anticipates the policy rate spread (currently 39bp) to disappear.

This current differential in expected pace of policy normalization appears largely due to differences in policy reaction functions priced by markets: As much focus as there has been on US disinflation, Canada’s inflation recent undershoot is as nearly as severe and as surprising: the cumulative core undershoot is very similar for both (1.5% in Canadian core CPI and US core PCE, having declined 0.5 over the past 9 months).

Only a handful of the analysts polled by Bloomberg expect a further Bank of Canada (BoC) rate hike today. All others, us included, believe that it will leave its key rate unchanged at 0.75%. The market reaction to the rate decision is going to be more pronounced than analysts’ forecasts suggest, as the market is pricing in a rate hike with a much higher probability (above 40%). So if the BoC was to leave everything unchanged today, CAD is likely to ease notably.

While Canada’s unemployment rate has fallen swiftly in the past 12 months (-0.7%-pts) it has remained roughly in-line with developments in the US (0.6%-pts), and BoC’s assessment is that there remains slack in Canada, whereas US is now well under NAIRU estimates.

While the US normalization cycle is well further along, historically Canadian rate cycles have lagged US ones and peaked at lower rates; In the past 20 years US-CA 2y spreads have never been negative in a tightening cycle (currently 7bp). A sustained narrowing of yields might be more convincing once the Fed does near the end of its tightening cycle, while BoC is still in the middle of its own. This is more likely to unfold after mid-18 and for that reason, and because of a projected 2H18 bounce in crude oil prices, we have CAD rebounding some to 1.30 in fresh 3Q’18 targets.

In particular, as its inflation outlook is based on stable exchange rates, but CAD is trading almost 6% above the level assumed by the BoC. Excessively aggressive rate hikes would risk an overshooting of the exchange rate.

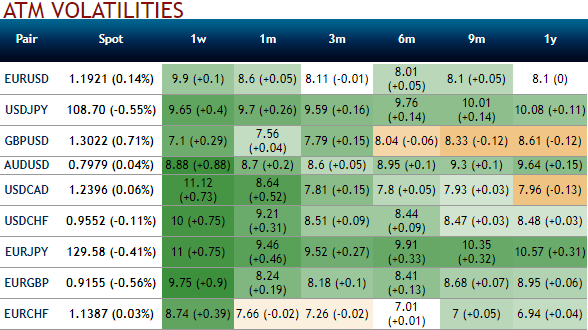

While the implied volatility remains among the three lowest G10 vols, seemingly options globally inexpensive. Despite the recent CAD appreciation, the USDCAD realized volatility has remained muted due to the low realized vol environment which makes knock-out barriers attractive.