FxWirePro- Woodies pivot (Major)

FxWirePro- Woodies pivot (Major)  FxWirePro: GBP/AUD dips ,remains on back foot

FxWirePro: GBP/AUD dips ,remains on back foot  GBPJPY Technical Check: Is the Dragon Running Out of Fire?

GBPJPY Technical Check: Is the Dragon Running Out of Fire?  FxWirePro: EUR/AUD drifts lower ,could be on verge of bigger drop

FxWirePro: EUR/AUD drifts lower ,could be on verge of bigger drop  FxWirePro= Major European Indices

FxWirePro= Major European Indices  Bitcoin Targets USD 90,000: Bullish Sentiment Solidifies as Realized Profits Surge

Bitcoin Targets USD 90,000: Bullish Sentiment Solidifies as Realized Profits Surge  FxWirePro: USD/CAD gains some momentum as weak Canadian jobs data weighs on loonie

FxWirePro: USD/CAD gains some momentum as weak Canadian jobs data weighs on loonie  FxWirePro: USD/CAD edges lower as oil rally strengthens Loonie

FxWirePro: USD/CAD edges lower as oil rally strengthens Loonie  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  NZDJPY Technical Outlook: Selling the Rallies as Bearish Momentum Consolidates

NZDJPY Technical Outlook: Selling the Rallies as Bearish Momentum Consolidates  FxWirePro: GBP/NZD dips towards 2.2800 level , vulnerable to more downside

FxWirePro: GBP/NZD dips towards 2.2800 level , vulnerable to more downside  FxWirePro: USD/ZAR slips as rand gains on weaker dollar

FxWirePro: USD/ZAR slips as rand gains on weaker dollar  FxWirePro: GBP/USD rises as UK political uncertainty fails to dent pound strength

FxWirePro: GBP/USD rises as UK political uncertainty fails to dent pound strength  CADJPY Outlook: Loonie Limps as Dismal Jobs Data Fuels BoC Rate Cut Bets

CADJPY Outlook: Loonie Limps as Dismal Jobs Data Fuels BoC Rate Cut Bets  FxWirePro: GBP/AUD edged higher, set to stay on back foot

FxWirePro: GBP/AUD edged higher, set to stay on back foot

- Why do put ladders seem better over put ratio spreads? - EconoTimes)

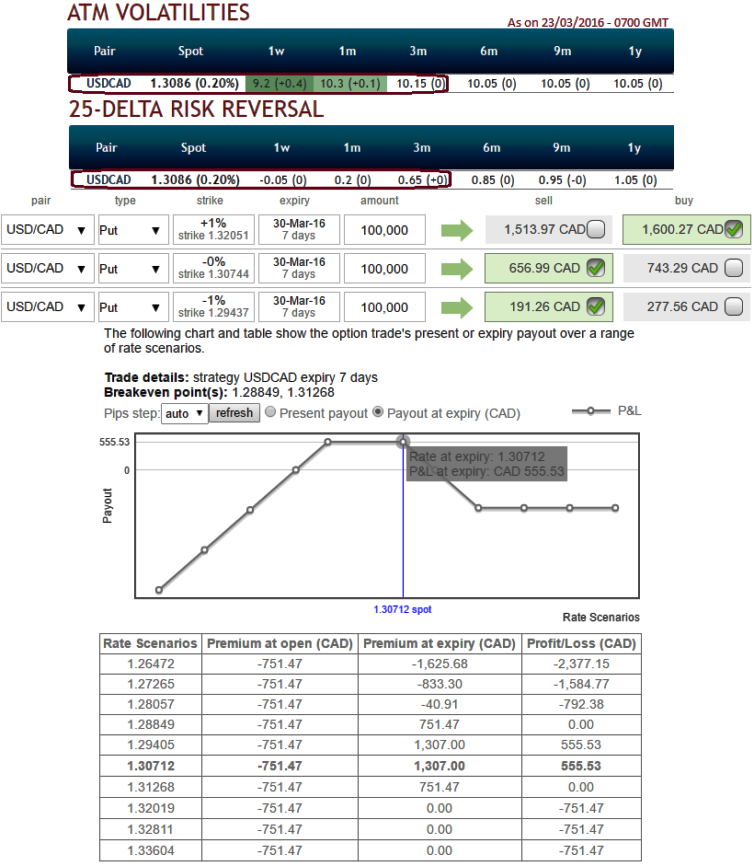

The implied volatility of USDCAD has been bullish neutral for 3M expiries among G7 currency segment contemplating risk reversal signals.

At spot ref: 1.3074, go long in 2M USD/CAD put ladder (strikes 1.3205/1.3074/1.2943).

Indicative offer: reduces cost about little more than 50% vs prem for ITM strike only.

The long put ladder is a limited returns and unlimited risk strategy as it proportionately employs more shorts in the spread because the underlying FX pair will experience little volatility in the near term (refer IV and risk reversal table).

Ideally, to execute this strategy, the options trader purchases an (1%) in-the-money delta put, short an at-the-money put and short another (1%) out-of-the-money put of the same expiration date.

Our put ladder is built as a standard put spread with tight strikes set at 1.3205/1.3074 financed by an OTM put with a strike at 1.2943.

Leaving only 125-130 pips between the former two strikes allows the profile to quickly reach the maximal possible leverage.

Unlike an usual put spread ratio, the maximal return is not reached on a given strike but over a wide region. It maximises the profitability of the trade via increased odds that the spot will trade in this region.

This short vega strategy is also short gamma so that an early spot depreciation will hurt the mark-to-market of the position.

Optimal leverage is only hit at the expiry and premature unwind is unlikely to be attractive before the two-thirds of the trade life.