Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

The USD rebound extended to the 1.3030 area yesterday, about where we think the short-term USD consolidation should run out of steam.

Soft trade data for November sustain the weak Q4 GDP outlook—Scotiabank Economics’ GDP Nowcast is tracking growth of virtually zero for the quarter currently, versus the BoC’s forecast of 1.3% in the last MPR. This is an important benchmark for policy makers and it remains to be seen whether BoC Gov Poloz remains as sanguine on the outlook in tomorrow’s comments from Vancouver as he was in Dec.

For now, we think CAD-supportive spreads and relatively firm crude prices can keep the USD advance in check certainly in the medium run. A dovish tilt to the governor’s comments tomorrow is a risk for the CAD, however.

Despite our expectations that Canada loses its cyclical exceptionalism and CAD unwinds some of its outperformance, the resulting currency weakness will be only modest, rather than large and broad.

Trading and Hedging Strategy:

Considering above underlying factors, we advocate 1% in the money put options of 2m tenors that seems to be the best suitable on hedging as well as trading grounds.

The rationale: USDCAD closed out 2019 on the defensive and made a crucial weekly/monthly close below long-term support zone of (1.2950 – 1.3165) drawn off the 2015-17 support zone for the USD on the longer run charts.

Although the pair has been attempting show some minor rallies from last 2-3 days, it is unwise to buck the major trend, interim rallies in the minor trend may be deceptive, and hence, we’ve considered ITM put options capitalizing on some driving forces. Below are the key factors listed out that drives us to prefer these derivatives instruments:

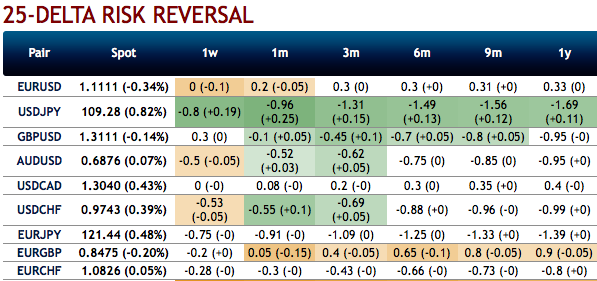

1) The bullish neutral risk reversal numbers indicate the inertia in hedging sentiments, while the underlying spot has been bearish (refer 1st chart).

2) While the positively skewed IVs of 3m tenors are indicating both the downside as well as upside risks (refer 2nd chart).

3) Please be noted that the payoff structure is quite handsome as it dips below 1.30 (BEP) (refer 3rd chart), hence, it is suitable for trading purpose also.

4) These ITM puts (2m) are fairly priced-in as they trading at CAD 1799, whereas Net Present Value (NPV) of these options are just 1713 which means they are trading at just shy above 5% and the IVs of 2m tenors are oscillating between 4.5 – 4.75% (refer 4th chart). Courtesy: Ore, Sentry, & Saxobank