Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics

LatAm currencies fought back against the idea that weaker global growth should cause them to weaken, and additional market pricing of Fed rate cuts undermined the broader USD and supported Latam currencies. Their rally was most likely exacerbated by investors’ light positioning in Latam currencies, as shown from CLP (typically a funding currency) outperforming MXN (which investors are net long according to CFTC data). Still, we do not such EMFX strength to last for much longer, particularly since next week market participants are likely to shift their attention back to China-US trade relations and the possibility of a “soft deal”.

As such, we maintain our Neutral Latam FX position, via OW BRL and COP, and UW MXN. In outright trades, we maintain our long BRL position via option structures, and a long PEN/CLP targeting 225.

Staying long as expected inflows from the oil reserve auctions should have a larger impact than SSR adjustments. The saga of the social security reform continues, and market participants were disappointed to find out that not only has the Senate passed an amendment that dilutes expected savings in the coming decade, but that the Senate has chosen to postpone its 2nd vote to October 22nd.

Nevertheless, portfolio flows and foreign positions should become less sensitive to these headlines, and increasingly focused on the Government’s privatization agenda and the possibility of foreign O&G firms buying BRL in order to participate in the excess oil auction due on November 6th.

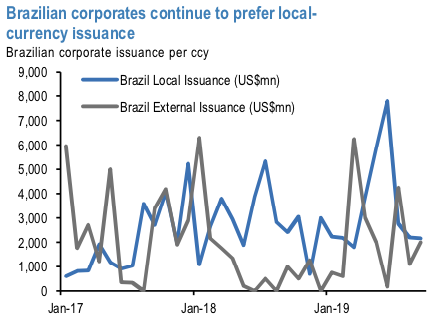

For now, weekly financial outflows continue to be the norm according to BCB data, and we remain aware that local corporates continue to prefer local-currency issuance over external: in fact, they continue to issue more in local currency, and have made additional USD-debt tenders for $2.6bn in September (refer above chart). Hence, we continue to recommend USDp/BRLc 1x2 option structures (K=4/4.20). Courtesy: JPM