How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Another upgrade to iron ore forecasts, recently, the iron ore analysts made some further upgrades to iron ore forecasts. A combination of stronger demand indicators in China and with weaker supply in 1Q is responsible for the forecast upgrades.

From 2Q, the quarter-to-quarter profile still marks a decline in iron ore prices over the course the year, as an eventual supply response emerges from higher cost suppliers and Chinese property sector demand moderates.

Our Q4’17 target for iron prices is now USD75/t (prior was USD66/t). On net, these revisions should lift our terms of trade profile by around 4%, and highlight ongoing under-valuation of the AUD REER (refer above chart).

On the flips side, we expect AUDUSD to decline through 2017 on skinnier rate differentials and a pull-back in commodity prices. Our Dec-17 target remains USD 0.71, in order to reflect risks of later rate cuts in Australia, but also to reflect the possibility that after 75bp of Fed rate hikes by 3Q17, the market might start to question the central bank’s ability to continue normalization of short rates.

This, along with significant uncertainty around the make-up of the FOMC in 2018, might represent a headwind to the USD towards year end.

By 1Q18, we forecast AUD to USD 0.69; even if the RBA does not deliver easing in 2H17, three hikes from the Fed will still leave minimal carry support for AUD, which is particularly important given its vulnerability to a turn in China’s momentum or adverse developments in global trade.

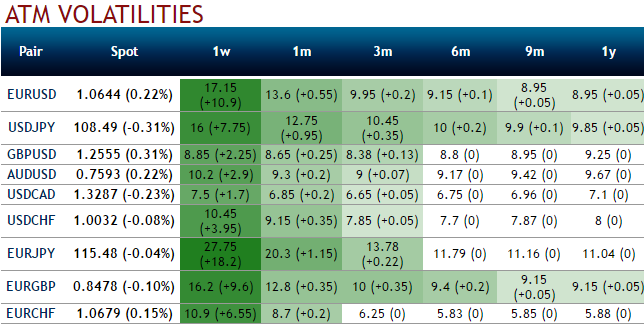

Please be informed that the nutshell showing negative risk reversals are bids for the hedging for the downside risks, as a result, puts are on more demands over calls. The negative risk reversals across all tenors are indicating the bearish hedging interests.

Please be noted that the 1w ATM puts are overpriced than prevailing implied volatility. 1w ATM puts priced 30% more than NPV, whereas 1w IVs are just below 10%. Hence, amid bearish-neutral risk reversals with this considerable disparity between IVs and option pricing we see an ideal shorting opportunity for option writers in overpriced OTM puts.

Option Trade Recommendation:

Weighing up above aspects, we eye on loading up with fresh longs for long-term hedging, more number of longs comprising of ATM instruments and ITM shorts in short term would optimize the strategy.

So, the execution of hedging positions goes this way:

Short 1w (1%) OTM put option as the underlying spot likely to spike mildly, simultaneously, go long in 1 lot of long in 1m ATM -0.49 delta put options and 1 lot of (1%) ITM -0.55 delta put of 2m expiry.