Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

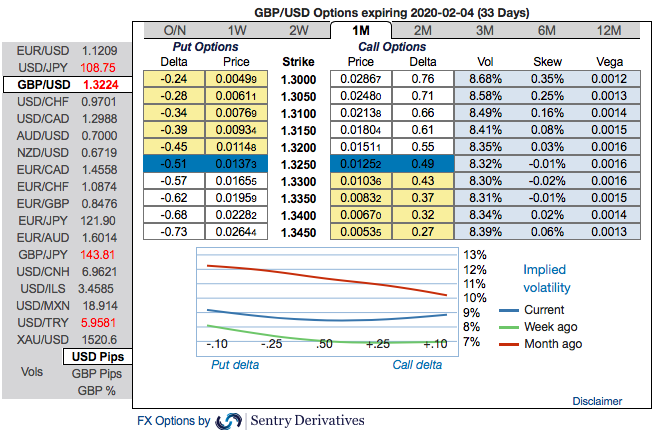

GBPUSD after pulling back from recent peaks of 1.3514, the pair has regained the buying momentum. The minor trend has taken trend line support at 1.2904 levels and spikes above 7 & 21-DMAs. On the balance, the structural setup for 2020 looks slightly negative for the USD early on. In the near term, analysts prefer to sell USD on rallies on the back of risk-on sentiment and a bearish technical setup. For now, we prefer to express a higher GBPUSD, EURUSD and AUDUSD. Meanwhile, the USDJPY we think may be clamped in by positive risk sentiment on one end, and a weaker USD on the other, leaving an overall range-bound posture.

The most bullish scenario for GBP given our assessment of these issues is likely to be a large Conservative majority, in line with the opinion polls. Yes this would deliver Brexit but Johnson would have the political wiggle room to dilute the relatively hard Brexit currently envisaged in the political declaration.

GBP's REER is cheap, 11% vs a 20Y average, but delivery of Brexit won't eliminate the bulk of the undervaluation. Much of this is as a consequence of the UK's worst-in-class current account deficit.

Central to the debate about GBP's prospective upside on a deal is the extent to which investors are U/W UK assets and over-hedged on GBP. We are cautious in assuming massive short-covering as visibility over aggregate position is low, while certain key investors such as reserve managers most definitely are not U/W.

GBP headroom is capped as investors have no clarity about the most important issue that will determine the economic consequences of Brexit - the future trade deal - albeit Johnson’s WA envisages a looser set of arrangements than May’s ill-fated deal.

Moreover, there is still the risk of an economic cliff- edge at the end of 2020 if Johnson honours his commitment not to extend the one-year transition.

Our assumption is that Brexit is the dominant issue for markets and so broader economic policies will be secondary for the exchange rate. GBP will likely take its directional cue from the read-through to Brexit whereas the size of the move will be augmented or moderated by the government’s broader policy platform.

Strategy (Debit Put Spread): Contemplating above factors, wise to deploy diagonal options strategy by adding short sterling via a limited loss tail hedge: Stay short a 1M/3W GBPUSD bear put spread (1.3425/1.27), spot reference: 1.3205 level.

The Rationale: Observe the 1m skews that has stretched on both the sides, hedgers have shown interests on both OTM Calls and OTM Put options. While the positively skewed implied volatilities of 3m tenors have still stretched towards OTM put strikes that indicates the hedging sentiments for the downside risks amid the minor upswings.

To substantiate the downside risk sentiment, risk reversal numbers have still been signalling bearish hedging sentiments. Hence, we advocate the diagonal options strategy on both hedging and trading grounds.