U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done

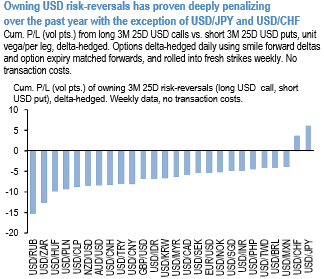

One of the most visible effects of this year’s dollar weakness is the relentless narrowing of risk-reversals in USD pairs, particularly since mid-Q2 once the French elections were out of the way.

Initially, softer riskies simply reflected a lowering of European political tail risks, but skew compression accelerated from June onwards as investor demand for USD puts – especially fueled by the Euro surge –pushed vols higher and turned the usual positive spot-vol correlation in USD pairs on its head.

Unsurprisingly, returns from owning delta-hedged USD riskies have been deeply negative owing to a mix of this surface re-pricing but more crucially smile decay: the above chart shows that the scale of the P/L penalty from owning USD calls over the past year far exceeds moves in implied vols alone.

Only two currencies – JPY and CHF –managed to buck the trend of unprofitable USD call ownership, less due to favorable directional moves over this and more because of earning smile theta with riskies priced in favor of USD puts in both cases. USDJPY may be a questionable candidate in light of brewing political risks in Japan, but USDCHF (3M 25D RR -0.8, 1Y -1.1) can act as a carry-positive overlay on bullish Euro positions and/or a hedge against an unexpectedly potent tax reform developments out of Washington. Courtesy: JPM