China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done

We raise 4Q’17 oil price forecasts by 4.50/bbl on Brent and $1/bbl on WTI to reflect the tighter balances now forecast, to $54.50 and $50.00/bbl, respectively.

Similarly, for 2018 we raise Brent to $47/bbl, and WTI to $43.25/bbl as we shift the assumption about how long OPEC-NOPEC will sustain production through to the end of 1Q'18. This keeps us bearish outright pricing, versus current spot and futures values, implying better value for producers to hedge output than for consumers to hedge fuel costs.

Yet, here again, we are reminded that the risks to the base case remain elevated, with geopolitical risks higher now than in many quarters. Moreover, market participants have had the luxury of ignoring risks presented from supply disruptions, while the market wrestled with oversupply and rapidly building inventories. Now that stocks are falling, such issues could come to grab the market’s attention. If the tail risks from either:

Iran, (possible new US sanctions),

Iraq (Kurdish secession risks prompt a suspension of exports from Turkish ports), or,

Venezuela –social situation deteriorates and production declines accelerate past that warranted by a lack of sufficient investment,

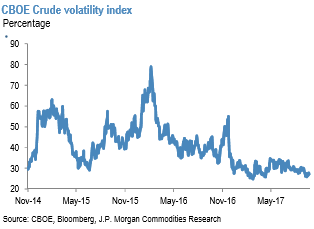

were to become the base case, prices could react in a manner that seems incongruous to a market with implied volatility trading close to three-year lows, (refer above chart).

The re-balancing is a result of strong consumption and also due to efforts led by the Organization of the Petroleum Exporting Countries (OPEC) to cut output by around 1.8 million barrels per day (bpd) in 2017 and the first quarter of next year. U.S. production hit 9.55 million bpd in late September, its highest level since July 2017 and not far off its 9.61 million bpd record from June 2015.

Geopolitical risks are higher now than for several quarters. The possibility of renewed US sanctions on Iran, the risk that Turkey may interrupt Kurdish exports on the back of increased secession risks and the continued social problems in Venezuela could all tighten markets in the short term. Moreover, market participants no longer have the luxury of ignoring risks from supply disruptions that oversupply and rapidly building inventories provided.

While we now assume that the OPEC deal will conclude at the end of 1Q’18 rather than the start, the big picture remains broadly unchanged from the views expressed in the 2017 outlook. Essentially, we continue to expect the OPEC deal to support prices in the short term, but we retain reservations about the implications for supply growth from higher prices, once the deal is unwound.

For further market guidance, it is worth keeping an eye on inventory data from the U.S. Energy Information Administration (EIA), which is due to be published later on Wednesday.