Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill

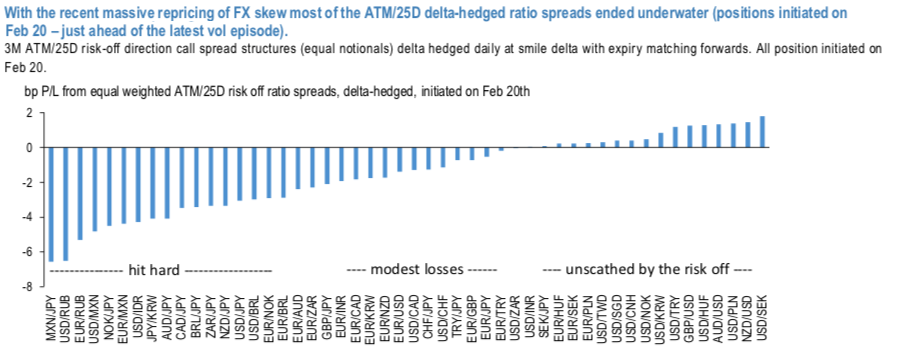

The entire global market sentiment has been driving strictly defensive positioning we think that it is prudent to keep an eye on historic skew dislocations their theta-scalping via risk off ratio spreads (delta-hedged). Those are a class of structures that can efficiently monetize excessive risk premia in vol smiles. While ratios can be struck for both calls and puts, the recent vol episode pushed the pricing of risk of OTM strikes into uncharted territory and made of particular interest the structures where the short notional is placed on the “risk-off” side, i.e. selling risk-reversals. While such structures are quicker in collecting premium, exposure to left tail is notable.

The brutal sell-off in crude oil prices as occurred over the past weekend led to a sharp repricing of vols and skews of oil-exporting currencies, most notably, RUB, NOK and CAD. A closer inspection reveals that outside of the EM petro-currencies and yen high beta crosses, the losses in risk-off ratio spreads were moderate (refer 1st chart). This is encouraging as the currently elevated levels of skew pricing should provide a buffer from incurring further losses if spot- vol correlation picks up again.

USDCAD vols risk-off call ratio spread is an outlier that dominates 2nd chart where currency pairs are screened based on 3-year Sharpe (a medium term performance horizon) of risk off ratio vol spread structures and 1y z-score of skew / ATM vol ratio.

3M USDCAD delta-hedged ATM/25D call spread @9.8/10.3indic vs 12.7ch, equal notionals to keep the structure net long vega.

An alternative way for benefiting from elevated skew, while offering at the same time risk-off exposure, is via directional (not delta-hedged) call spreads. Especially in the case of CAD, a regression analysis finds that the latest move in Oil well justifies the changes in vol and skew, but that there is further room for spot to move higher (about +3% of upside based on the past 3m change in Oil prices).

Consider: 3M USDCAD 1.40/1.4280 strikes (40D/30D) call spread (live, no delta-hedge) costs @55bps USD (spot ref. 1.3860), 3.5X max payout / cost ratio. Courtesy: JPM