China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations  BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks

BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks  Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027

Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

Following the end of the rate hike cycle in Mexico, the markets are now speculating when the first rate cut may follow. Against this background, today’s publication of the inflation report, as well as a speech by central bank governor Augustin Carstens, are of interest. In view of the still high inflation rate of 6.4% speculation of this nature seems premature to us though.

We believe that the central bank will no doubt want to be sure that inflation is moving towards the inflation target of 3% in a sustainable manner before taking a first rate step, and as a result we expect a lengthy rate pause. That means there is unlikely to be any momentum for the peso on this front. Instead, the NAFTA renegotiations might stir things up a little bit for the currency.

The second round of negotiations is scheduled at the end of this week. However, (negative) effects on the peso are likely to be limited. Recent comments on the part of US President Donald Trump, which once again suggested that the agreement might come to an end, only put short term pressure on the peso. The general point of view that the agreement is likely to remain in place in the future was not affected by this sabre rattling.

But investors may become a little more nervous and take a cautious approach towards MXN engagements. USDMXN is likely to trend sideways again in the near future.

The peso has come a long way from its Trump lows and screens overbought and overvalued at current levels, leading our LatAm team to turn underweight recently.

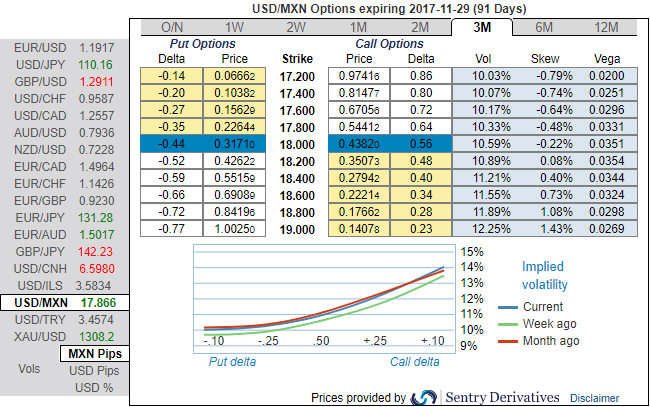

The standout feature of the USDMXN vol surface to us is the cheapness of risk-reversals, both vis-à-vis ATM vols and particularly relative to the amount of carry in forwards that allows for carry efficient expressions of bearish directional views or tail risk hedges.

Please be noted that the 3m IVs of USDMXN are indicated bullish risks, the telling statistic from the graphic is that that the static carry of delta hedged vega-neutral 3M skews is a very substantial 2.5 vol pt., near the upper-end of its 2-yr range.