Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

Data events: BoC Gov Poloz speech on 28th March.

Canadian GDP on 31st March.

Aussie Retail Sales on 2nd April.

Aussie Trade balance on 3rd April.

RBA’s Monetary Policy on 4th April.

Canadian Trade balance on 4th April.

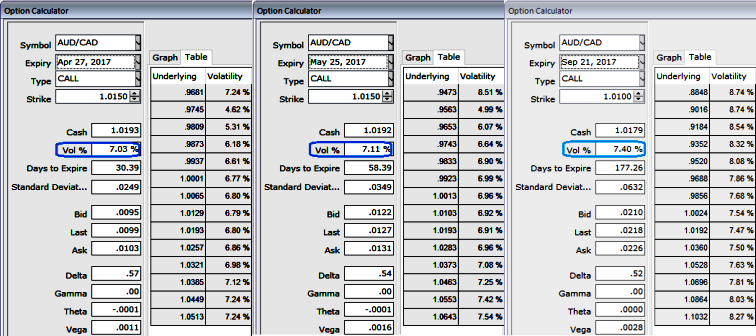

Please be noted that the implied volatilities of AUDCAD have been extremely lackluster, crawling at shy above 7% for 1m tenor and 7.11% for 2m tenor despite the flurry of data announcements as stated above.

AUDCAD 6M vols appear decent buys given their depressed levels (not far from 2014 lows) and the uber flatness of the 3M-6M vol curve.

Realized vols are not stellar however in a dollar-centric environment; hence theta bleed on vol longs is best avoided via forward volatility (FVA) structures.

So, opening positions in OTM AUD puts/CAD calls to monetize a potential correction lower in the cross is the clean directional play; one can for instance consider buying 6M 0.91 AUD puts/CAD calls with leverage in excess of 5:1 as a medium-term bearish play, where the admittedly distant barrier (8% OTMS) is still within the realm of possibility, having been breached only last September after the CNY devaluation.

Alternatively, relative value constructs involving buying AUD puts/CAD calls vs. selling USD puts/CAD calls (live, no delta-hedge) appeal as low cost ways of assuming exposure to the same directional dynamic.

The above chart demonstrates that OTM AUD puts/CAD calls are historically cheap and discounted in vol (and premium for the same delta) relative to OTM USD puts/CAD calls, which is odd because their spread behaves like an anti-risk asset by virtue of effectively being short AUDUSD delta, and hence ought to command a net positive premium.

Cumulative P/Ls from owning 6M 25D AUD put/CAD call – 6M 25D USD put/CAD call option spreads (bp CAD), and 6M 25D AUD puts/USD calls.

All options live (not delta-hedged) and rolled into fresh strikes monthly. Shaded bars represent vol spike episodes. No transaction costs.

The anti-risk nature of the AUDCAD – USDCAD option spread: it essentially mimics returns from an equivalent tenor/delta AUD put/USD call – but at a fraction of the cost of the latter and with outperformance in periods of calm when time decay is a drag on the latter.

The risk to the spread is evidently a major USD sell-off that hurts USDCAD significantly more; the working assumptions are:

(a) This is unlikely to materialize in the lead up to the June FOMC, and (b) the risk of an upward drift in G3 rates poses upside risk for the greenback against lower quality EM FX that should keep a lid on large scale dollar washouts.

From a trade structuring standpoint, we also create some cushion against USD declines by striking options meaningfully out of the money (25D) such that local, small scale dollar weakness has low odds of filtering through to terminal option returns.