FxWirePro: EUR/ NZD gaining momentum for a move towards 2.0350 level

FxWirePro: EUR/ NZD gaining momentum for a move towards 2.0350 level  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  ETH Bounces as Shorts Cover, Yet ETF Bleed Warns $1,850 Resistance Won’t Break

ETH Bounces as Shorts Cover, Yet ETF Bleed Warns $1,850 Resistance Won’t Break  AUDJPY Bears Take a Breather at 111.50, But ‘Sell on Rallies’ Still Eyes 110

AUDJPY Bears Take a Breather at 111.50, But ‘Sell on Rallies’ Still Eyes 110  FxWirePro: GBP/AUD edges higher but bullish outlook persists

FxWirePro: GBP/AUD edges higher but bullish outlook persists  FxWirePro:GBP/USD recovers slightly from early decline but bears are not done yet

FxWirePro:GBP/USD recovers slightly from early decline but bears are not done yet  FxWirePro- Woodies pivot (Major)

FxWirePro- Woodies pivot (Major)  AUDJPY Under Pressure: US Dollar Strength and Bearish Technicals Signal Further Declines

AUDJPY Under Pressure: US Dollar Strength and Bearish Technicals Signal Further Declines  Bitcoin Sheds $491M in ETF Outflows and Retreats Below $64K; Sellers Reload for $50K

Bitcoin Sheds $491M in ETF Outflows and Retreats Below $64K; Sellers Reload for $50K  NZDJPY's Downward Spiral: Will 92 Resistance Seal the Bearish Fate?

NZDJPY's Downward Spiral: Will 92 Resistance Seal the Bearish Fate?  FxWirePro: USD/CAD loses momentum but bullish setup remains

FxWirePro: USD/CAD loses momentum but bullish setup remains  NZDJPY Bears Reload as 92 Resistance Caps Bounce; Sell-on-Rallies Eyed Toward 90

NZDJPY Bears Reload as 92 Resistance Caps Bounce; Sell-on-Rallies Eyed Toward 90  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  EURJPY Consolidates Above Key EMAs: Mixed Indicators Suggest Cautious Optimism for Traders

EURJPY Consolidates Above Key EMAs: Mixed Indicators Suggest Cautious Optimism for Traders  FxWirePro: USD/CAD uptrend loses steam, remains on bullish path

FxWirePro: USD/CAD uptrend loses steam, remains on bullish path  GBPJPY Caught in a Tight Range: Bearish EMAs Suggest a Breakout Awaits

GBPJPY Caught in a Tight Range: Bearish EMAs Suggest a Breakout Awaits

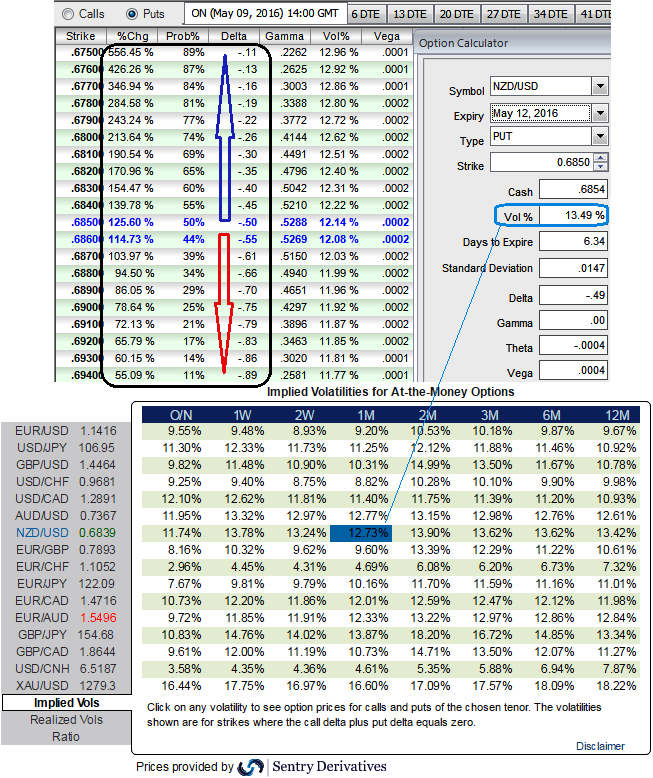

The AUD and NZD remained in a holding pattern ahead of today’s RBA statement plus US jobs report, while US interest rates fell. The US dollar index (DXY) rose by around 0.7% overnight, while NZD ranged between 0.6876 and 0.6918.

ATM IVs of 1W expiries are at 13.49% and 12.73% for 1M tenors, so it has reduced a bit, however the volatilities implied in FX option market of this pair is likely to perceive higher volatility times even after monetary policy season in both NZ and US continents which is good news for option holders.

Now, let’s glance on the sensitivity table for %change in every rise in OTM strikes and their probabilities, which means that higher chances of these strikes expiring in the money are very high.

Because, the higher volatility would mean that the option price has moved or is expected to move over a larger range in a set time period.

Subsequently, have glance on sensitivity table as well for the different rate scenarios and their probabilistic outcomes. We've just referred 0.25% OTM put strikes and their vols, it still shows 0.47 as delta values for underlying outrights with 52% of probabilities, that means 52% chances of finishing in-the-money.

Three months ahead we see markets pricing in further RBNZ easing (below 2.0%), and also pricing a greater chance of US Fed rate hikes. The NZ-US interest rate outlook thus argues for a lower NZD/USD, towards 0.6500.

As you can see the %change in option strikes and their prices, the options of ITM strikes are the most expensive. So buyers would pay the most and sellers would receive the most. Their premium is mostly made up of intrinsic value so they are relatively immune to Vega and Theta.

Vega is stagnant on either side, hence, trade an ITM option if you want to minimize the risk of Vega and Theta. They are an excellent tool when you have a strong view on the market because deep ITM options have the highest Delta. They will behave more like a position in the underlying.

On the flip side, OTM options are always the cheapest options hence buyers pay less and sellers receive less. They rely solely on extrinsic value and have a low Delta, Theta, and Vega. A move towards the ATM territory increases the Vega, Gamma and Delta which boosts premium.

Hence, OTM put options are the best suitable for those we seek long term hedging instruments for further downside risks and ITM options for short term.