World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum

Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch

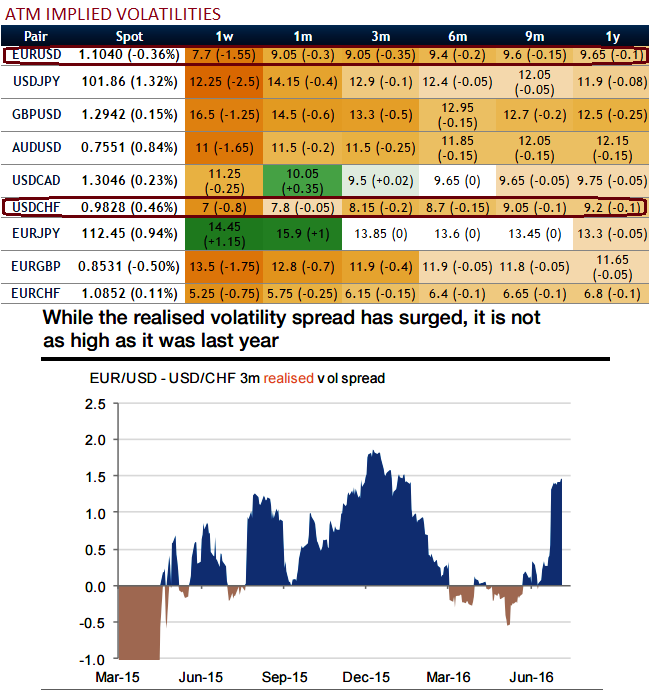

Further divergence between EUR/USD and USD/CHF volatility A spread of volatility swaps is exposed to the volatility differential between two currency pairs. Investors holding the position until the 3m expiry face unlimited losses if the realised volatility between EUR/USD and USD/CHF eventually exceeds 0.7 vols.

As we expect the vol spread to converge towards a flat level, it is advisable to go long in USD/CHF vs shorts in EUR/USD 3m volatility swaps, indicative bid: receive 0.7 vols.

However, past patterns suggest that the realised vol of the spread could exceed 0.7 vols (see above graph).

As such, we recommend unwinding the position before the expiry as soon as the net profit exceeds 0.5 vols.

Long/short of volatility swaps as a pure volatility trade, we recommend getting a pure volatility exposure via a long short of volatility swaps.

It allows for getting rid of systemic delta hedging and more generally of most of the gamma risks.

The pay-off of these instruments depends on realised volatility but their market to market (vega) is sensitive to implied volatility as well.