Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

Very recently, the British Foreign Secretary Boris Johnson will hopefully not take it personally that Sterling appreciated briefly yesterday in reaction to reports he might resign. We interpret the exchange rate moves in such a way that Sterling will benefit whenever the likelihood of Great Britain continuing to enjoy far reaching access to the European single market rises.

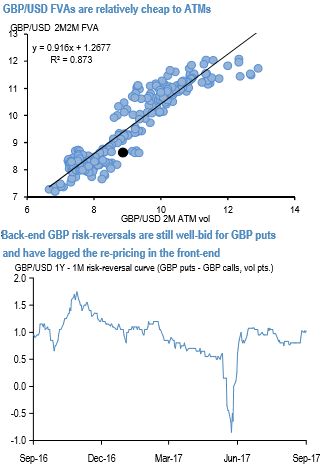

There exists a couple of option build ups that appear worth chasing after the post-Vlieghe run-up in GBP vol from a value standpoint. First, liquidity permitting, GBPUSD 2M2M FVAs offer 0.75 vols of RV edge on mids vis-à-vis 2M ATMs (refer above chart), carry flat-to-mildly positive along the vol curve and are potentially floored on P/L even if spot were to begin to consolidate if we are right that the state shift higher in implied vol is here to stay.

Second, backend (6M-1Y) GBP risk-reversals have lagged the repricing in the front-end, where skews have already flipped in favor of GBP calls in 1M and under expiries (refer above chart). While the bearish neutral risk reversals of 3m tenors indicates the bearish risks remain intact in the long term.

This is a perfectly rational market response to recent news flow, but one that should gradually adjust over time as the skew move propagates out the curve while rewarding shorts with positive smile theta along the way.

On similar skew grounds, buyers of GBP vega are best advised to install longs in the 6M-9M tenor 30D-35D strike GBP calls that represent the trough of the vol surface in most GBP pairs; directional investors sympathetic to our bearish AUD outlook might even consider 6M30-35D GBP call – AUD call option spreads as an expression of GBP bullishness while exploiting vol surface RV that makes GBP calls relatively cheap to AUD calls. We have even stated in our recent post that the cheap GBP valuations on some longer-term metrics. The additional 1.5% weakening in GBP in response to the election has made GBP the second cheapest currency globally on a REER basis

The reports of Boris Johnson standing down were due to the fact that Prime Minister Theresa May might suggest a Swiss model in her eagerly awaited Brexit speech 2.0 on Friday which would allow Great Britain to buy the right to (partial) access to the single market with contributions to the EU budget. Even though Sterling was unable to maintain the gains, yesterday’s developments illustrate that GBP investors are focused on May’s speech on Friday. Against this background today’s retail data is likely to fade into insignificance.