U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

The EUR remains subdued due to Italian budget risks. Meanwhile, today’s ECB minutes will be scrutinised for clarity regarding the additional comment in their post meeting statement which referred to the risks to the economy from protectionism and emerging markets.

We look for options constructs for hedging EUR weakness in case where Italian yields were to rise further. We like considering maturities of around 2M for allowing for the budget to be officially released by the government, voted by the Italian parliament and later reviewed by the EU, in a back and forth process which could extend until the end of November. The fact that EUR vols reacted just modestly to the announcement of the Italian budget makes the entry point of the trade attractive, in our view.

One can further look to cheapen a long vol structure by introducing a correlation element to it. In refer 1st chart, we consider the time series of pair-wise implied EUR- correlations of CHF, JPY and USD. Current levels of 2M implied correlations don’t stand as dramatically undervalued (at 58% on average), but haven’t spiked on the Italian budget news either. By considering a set of triplets of EUR-crosses in the G7 space, we would find that in a worst-of put structure, JPY, CHF and USD would be the one offering the least correlation discount (60%) vs the cheapest plain vanillas.

By choosing the CHF, SEK, USD triplet, for instance, the correlation discount could rise to 80%, but the sensitivity to the BTP-Bund spread would typically find EUR to appreciate vs SEK on a higher level of spread, thus making the latter currency less suitable to be included in a EUR hedge trade.

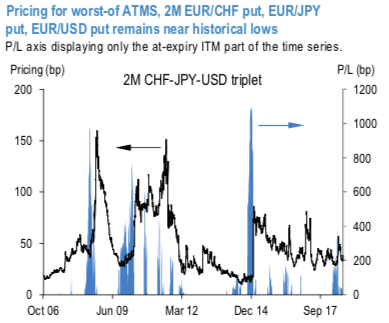

The pricing of the structure remains competitive from a historical perspective (refer 2nd chart, with the trade often delivering large PnL on the back of jumps in vols and/or correlations (with max leverage >10 times).

We opt for 2% OTMS strikes for further cheapening the premium and structuring it as a proper tail-risk hedge. We consider 2M, 2% OTMS worst-of EURJPY put, EURCHF put, EURUSD put at 14/18.5 bps.

Alternatively, one could consider an implementation via dual-digitals involving just two EUR-crosses. Amongst the most sensitive EUR-crosses against the Italian yields, EURCHF lower EURUSD lower is the combination offering the highest maximum leverage (around 9 times). Courtesy: JPM

Currency Strength Index: FxWirePro's hourly EUR spot index is flashing at 79 levels (which is bullish), while hourly USD spot index was at -105 (bearish) while articulating at (11:06 GMT). For more details on the index, please refer below weblink: