Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data

As you could see EURJPY 6m implied volatility too elevated, as it is unsupported by both 6m and 1m realized volatilities suggesting a decent risk premium to be monetized.

The variance swap recommended above expresses our views in the volatility space. Investors desiring to get a directional bullish exposure in EURJPY can take advantage of the current volatility surface confirmation by buying a topside seagull that is short both the excessive volatility and skew.

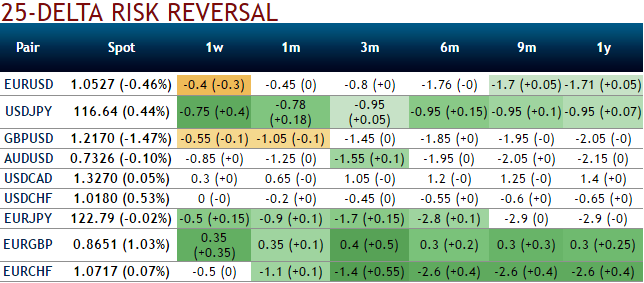

Relative value in the EURJPY volatility surface strongly suggests selling 6m and 1y low strikes, which are now valued at a premium above the shorter tenors. The RR curve strongly steepens beyond the 3m expiry, and the corresponding RR levels are trading above their median level, unlike the shorter segment (see above graph).

We recommend buying a EURJPY 6m call spread about one figure out of the money and with a strike width slightly exceeding four figures. This strategy can be fully financed by selling a 25-delta put. In terms of levels in current conditions, it amounts to buying a topside seagull with strikes 114/123.5/128.

This structure appears to be more appropriate when volatility is high but likely to likely to shrink, and the price is expected to trade with a lack of certainty on direction. Despite the limiting yields since they are spread structures rather than vanilla structures ITM longs would give magnifying impact in the payoffs.