SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025

, it is a halt? - Diagonal tenors in “long put ladders” to fetch certain yields even in choppy range - EconoTimes)

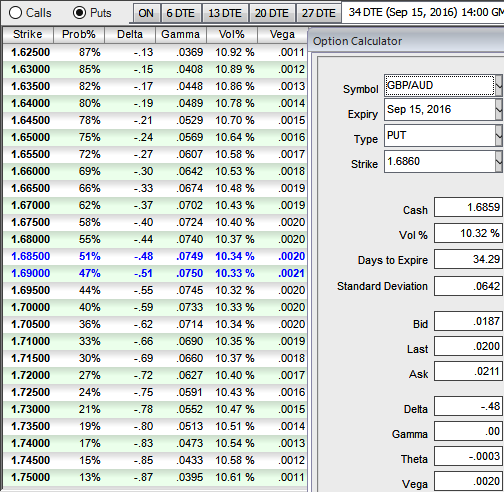

As stated in our earlier post on this pair’s technical lines, bears have extended slumps below 61.8% Fibonacci retracements and major downtrend still seems bearish despite abrupt upswings.

You can refer below weblink for more reading on technicals:

So any price bounces should not be deemed as a recovery in the major downtrend, instead one can capitalize these upswings to deploy fresh short build ups.

The implied volatility of GBPAUD has been bullish neutral for 1M expiries contemplating risk reversal signals.

At spot ref: 1.6859, go long in 2M/1W/2W GBPAUD put ladder (strikes 1.7667/1.6859/1.6525).

Indicative offer: reduces cost about little more than 50% vs prem for ITM strike only.

The long put ladder is a limited returns and unlimited risk strategy as it proportionately employs more shorts in the spread because the underlying FX pair will experience little volatility in the near term (refer IV and sensitivity table).

Ideally, to execute this strategy, the options trader purchases an (1%) in-the-money delta put, short an at-the-money put and short another (1%) out-of-the-money put of the same expiration date, however this’s not hard and fast, one can choose strikes as per his priorities.

Leaving only 100-125 pips between the former two strikes allows the profile to quickly reach the maximal possible leverage.

Unlike an usual put spread ratio, the maximal return is not reached on a given strike but over a wide region. It maximises the profitability of the trade via increased odds that the spot will trade in this region.

This short vega strategy is also short gamma so that an early spot depreciation will hurt the mark-to-market of the position.

Optimal leverage is only hit at the expiry and premature unwind is unlikely to be attractive before the two-thirds of the trade life.