Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  BOJ Policymakers Warn Weak Yen Could Fuel Inflation Risks and Delay Rate Action

BOJ Policymakers Warn Weak Yen Could Fuel Inflation Risks and Delay Rate Action  Bank of Canada Holds Interest Rate at 2.25% Amid Trade and Global Uncertainty

Bank of Canada Holds Interest Rate at 2.25% Amid Trade and Global Uncertainty  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Why Trump’s new pick for Fed chair hit gold and silver markets – for good reasons

Why Trump’s new pick for Fed chair hit gold and silver markets – for good reasons  Fed Governor Lisa Cook Warns Inflation Risks Remain as Rates Stay Steady

Fed Governor Lisa Cook Warns Inflation Risks Remain as Rates Stay Steady  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  ECB’s Cipollone Backs Digital Euro as Europe Pushes for Payment System Independence

ECB’s Cipollone Backs Digital Euro as Europe Pushes for Payment System Independence  China Extends Gold Buying Streak as Reserves Surge Despite Volatile Prices

China Extends Gold Buying Streak as Reserves Surge Despite Volatile Prices  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

JPY has been a middle-ranked but relatively weak currency within the G10 camp. Meanwhile, developments in the recent past:

1) An unexpected dovish turn by the Fed at the January FOMC resulting in a bearish view on USD,

2) The heightened concerns over the outlook of the global economy in favor of a bullish JPY view, and

3) The growing speculation that there will be upward pressure on JPY due to repatriations towards end-FY2018 (March 2019).

These factors, however, have likely supported the JPY bottom.

After a short-lived flash crash spike at the turn of the year, Yen vols have resumed their downtrend and are well on their way to testing their lows from 2Q’14 (refer 4th chart). The break of 8.0 on USDJPY 1Y ATM vol back in December had caused a frisson of excitement among vol accounts looking to buy Yen vega as a strategic late cycle FX vol play, but what was deemed to be a key technical support level has long since been left in the dust. 7.0 now looms as the next major target, beyond which there is still substantial room to fall to revisit pre-GFC levels in the 6s.

It is difficult to argue with option prices steadily softening when the spot is stuck in a tight 109-111 range and delivering 2-2.5 pts. below implieds.

There is also a case to be made that the ongoing softness in realized vols can continue longer than some anticipate, since the propensity of the Yen to rally in market downturns is being dampened by a cyclically wide US-Japan interest rate differential that is fuelling above-average equity and FDI outflows, alongside a reduction in FX hedge ratios of traditionally well-hedged foreign bond purchases.

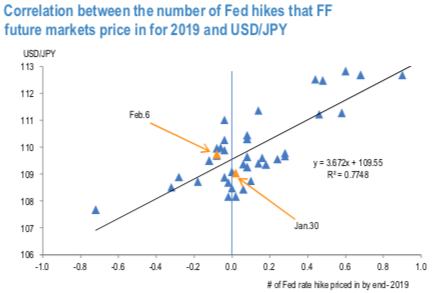

The number of Fed hikes that the FF future markets are pricing in for 2019 has continued to have a relatively strong correlation with USDJPY (refer 1stchart). FF future markets did not price in any hike even before the FOMC on January 30th.

The BoJ introduced a negative interest rate policy in end-January but this was

not sufficient to counter the deterioration in global risk sentiment. Also, it is worth noting that these developments led to the revision of the policy rate forecast at the March FOMC in 2016. Separately, Japanese investors net-sold foreign stocks and investments funds in April after entering into the new FY, following the global stock sell-off (refer 2nd chart). Meanwhile, Japanese investors remained net buyers of foreign bonds in this period— likely accompanied by JPY selling (refer 3rd chart). In 2018, JPY appreciated amid a rapid rise in VIX and global stock sell-offs in February and March. Japanese investment trusts also net-sold foreign stocks and investments funds in February and March, which might have contributed to the acceleration in JPY appreciation. Courtesy: JPM

Currency Strength Index: FxWirePro's hourly USD spot index was at 49 (which is bullish), while hourly JPY spot index was at 29 (bullish) at 07:18 GMT.

For more details on FxWirePro's Currency Strength Index, visit http://www.fxwirepro.com/currencyindex