U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

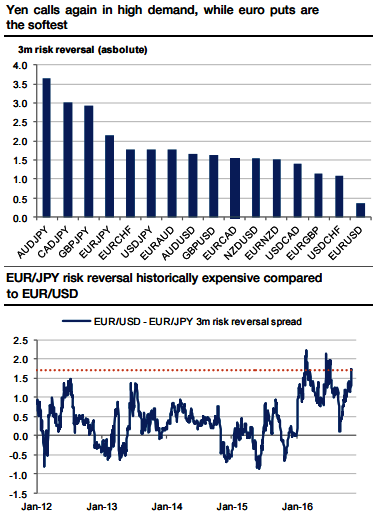

The excessive yen skew premium Yen calls are in high demand for all crosses (see above graph) as the market is behaving in a risk-off way. As we wrote here and here, the yen probably met an inflexion point after months of strength.

It is bid this week just ahead of the election, but a Clinton victory remains the central scenario and would provide immediate relief.

A Trump victory would pressure the USDJPY towards 100 but a break would not at all be to the BoJ’s taste, whereas the Fed is edging closer to a December hike, making a new rebound likely. Selling outright yen volatility or skew is not a reasonable trade given the imminent risk event, but selling the yen skew premium as a leg of a relative value trade appeals.

Stay short EURJPY rather than USDJPY skew, the EURJPY 3m skew is larger than the USDJPY skew (-2.1 vs -1.8), so that selling the former provides a higher premium.

Moreover, the EURJPY skew exceeding the USDJPY is not consistent in times of EUR topside volatility. On the contrary, euro bullishness should dampen the EURJPY skew, which is, therefore, an attractive Sell.

The spread between EURJPY and EURUSD 3m risk reversals is now very elevated historically, as it is exceeding 1.5 vols (see above graphs).

It never happened between 2012 and 2015 and such a situation happened only very transitorily this year. We expect the gap between EURJPY and EURUSD skews to tighten.