Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Jerome Powell Attends Supreme Court Hearing on Trump Effort to Fire Fed Governor, Calling It Historic

Jerome Powell Attends Supreme Court Hearing on Trump Effort to Fire Fed Governor, Calling It Historic  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Bank of Japan Signals Cautious Path Toward Further Rate Hikes Amid Yen Weakness

Bank of Japan Signals Cautious Path Toward Further Rate Hikes Amid Yen Weakness

Amid the prevailing risks for the slowdown in the global economy, the yen is, on the one hand, in demand as a safe-haven, while on the flip side, it is likely to become more and more obvious in the course of the easing efforts of other central banks that the Bank of Japan will hardly be able to further ease its monetary policy in a credible manner.

Conceptually, the BoJ would have to stop buying bonds at the long end, or even sell JGBs, to defend its yield target. But in light of an inflation that remains close to zero that would be a totally inappropriate restrictive signal which would likely increase the appreciation pressure on the yen substantially. The BoJ recently reduced its purchases at the long end slightly, but there was no significant effect on the yield curve. And at the short end, downside potential is limited by the key interest rate. Since the Bank of Japan has included the cost considerations for the financial sector in its monetary policy decisions, a further permanent easing of Japanese monetary policy - to the extent that it is possible at all - is not credible. Instead, the market will always quickly speculate on a possible normalisation of monetary policy as soon as the economic environment brightens even a little - which would then allow the yen to appreciate again.

In relative terms, the BoJ thus threatens to become more restrictive, especially compared to the Fed, which is why we expect the yen to appreciate significantly against the USD. Since the European central bank (ECB) is also in a similar dilemma to the BoJ and its monetary policy arsenal has practically dried up, we expect EURJPY to move broadly sideways in the near-terms while the major downtrend remains intact. ECB is scheduled for their monetary policy next week.

Contemplating all these underlying factors, euro seems to be edgy on increasingly chronic underperformance of the Euro area economy. We could foresee reasonably bearish risks for EURJPY amid such backdrops.

OTC outlook (EURJPY): We noted in our recent post that the positively skewed IVs of 3m tenors signifying the hedging interests for the downside risks. There is no much change in our hedging outlook, as the bids for OTM puts expect that the underlying spot FX likely to show further dips so that OTM instruments would expire in-the-money.

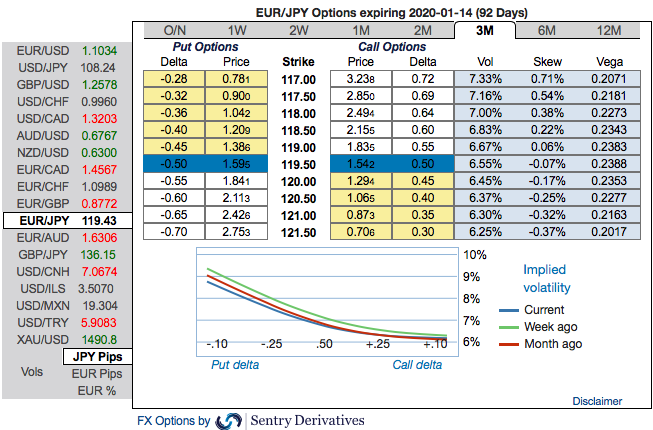

Most importantly, to substantiate the above indications, we could see some minor positive shifts in existing bearish risk reversal set-up of EURJPY that indicates the long-term hedging sentiments across all tenors are still substantiating bearish risks amid minor abrupt upswings in the short-term. Please be noted that 3m IVs are overall OTC barometer is noteworthy size in the forex options market that can stimulate on the underlying forex spot rate.

Options Strategy: Contemplating above factors, we’ve advocated buying 3m EURJPY (1%) ITM -0.79 delta puts for aggressive bears on hedging grounds as the mild abrupt upswings were contemplated earlier.

Short hedge: Alternatively, we advocated shorts in futures contracts of mid-month tenors with a view to arresting potential dips. since further price dips are foreseen we would like to uphold the same strategy by rolling over these contracts for September month deliveries. Source: Sentrix, Saxo & Commerzbank