FxWirePro : AUD/USD drifts lower, could be on verge of bigger drop

FxWirePro : AUD/USD drifts lower, could be on verge of bigger drop  FxWirePro : GBP/NZD uptrend loses steam, remains on bullish path

FxWirePro : GBP/NZD uptrend loses steam, remains on bullish path  EURUSD Bullish Momentum: Trading Above 800, 365 EMAs with Positive CCI on 5-Min Chart

EURUSD Bullish Momentum: Trading Above 800, 365 EMAs with Positive CCI on 5-Min Chart  FxWirePro: USD/CAD loses momentum but bullish setup remains

FxWirePro: USD/CAD loses momentum but bullish setup remains  AUDJPY Under Pressure: US Dollar Strength and Bearish Technicals Signal Further Declines

AUDJPY Under Pressure: US Dollar Strength and Bearish Technicals Signal Further Declines  FxWirePro: GBP/USD neutral in the near-term, scope for downward resumption

FxWirePro: GBP/USD neutral in the near-term, scope for downward resumption  EURJPY Consolidates Above Key EMAs: Mixed Indicators Suggest Cautious Optimism for Traders

EURJPY Consolidates Above Key EMAs: Mixed Indicators Suggest Cautious Optimism for Traders  FxWirePro: NZD/USD extends losing run, eyes 0.5600 level

FxWirePro: NZD/USD extends losing run, eyes 0.5600 level  FxWirePro: USD/CAD uptrend loses steam, remains on bullish path

FxWirePro: USD/CAD uptrend loses steam, remains on bullish path  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  FxWirePro: USD/ZAR retreats slightly but trend is still bullish

FxWirePro: USD/ZAR retreats slightly but trend is still bullish  FxWirePro: USD/JPY dips as Japanese Yen consolidates near 40-year low

FxWirePro: USD/JPY dips as Japanese Yen consolidates near 40-year low  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  FxWirePro: EUR/ NZD gaining momentum for a move towards 2.0350 level

FxWirePro: EUR/ NZD gaining momentum for a move towards 2.0350 level  FxWirePro- Woodies pivot (Major)

FxWirePro- Woodies pivot (Major)  Bitcoin Sheds $491M in ETF Outflows and Retreats Below $64K; Sellers Reload for $50K

Bitcoin Sheds $491M in ETF Outflows and Retreats Below $64K; Sellers Reload for $50K

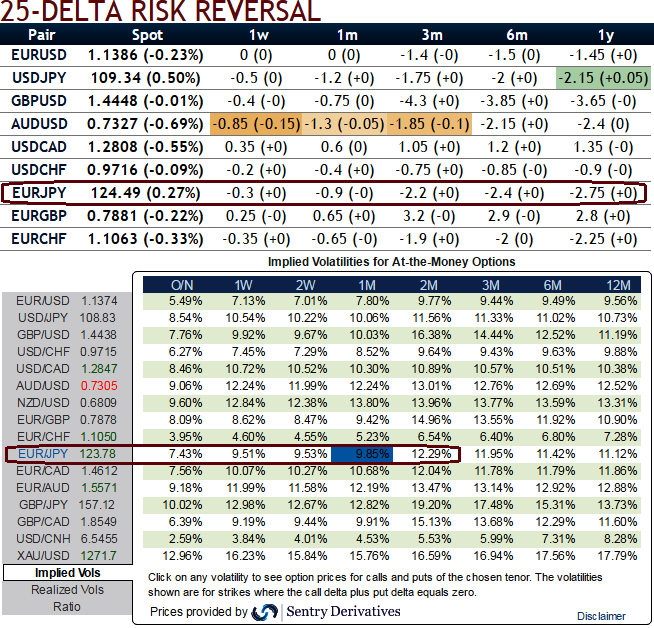

Technicals Watch: This week’s price bounces have now tested and rejected resistance at 124.445 levels (daily charts), that’s where a “Shooting Star” pattern occurs, as a result, we see bears resuming again, current prices testing supports at 123.6212 (21DMA), slide below 21DMA to bring in more slumps. On a broader perspective, the current prices remain below EMAs despite attempts of bounces; downtrend has been slipping through falling wedge formation on monthly charts.

OTC Updates: The implied volatility of ATM contracts is at 9.51% for 1w expiries and inching higher at 9.85% for one month tenors which is edging higher again in long run.

As you can see delta risk reversals are indicative of participants in this pair are more concerned about further slumps especially from next 3 months timeframe. Rising negative flashes indicates active hedging sentiments for these downside risks.

25-delta risk reversal reveals the difference in volatility, and therefore price, between puts and calls on the most liquid out-of-the-money (OTM) options quoted on the OTC market, subsequently, the put are the expensive comparatively to the calls.

Acknowledging the gradual increase in the implied volatility of EURJPY but with higher negative risk reversals in long run is justifiable when you have to anticipate forwards rates and observe the spot curve of this pair (see IVs, RR nutshell, Sensitivities, and compare with spot prices).

Major trend is declining trend, from last two years or so the pair has consistently evidenced price slumps more than 17%, and we could still foresee more downside potential ahead.

Hedging Positioning:

Weighing up above aspects, we eye on loading up with fresh longs for long term hedging, more number of longs comprising ATM instruments and ITM shorts in short term would optimize the strategy.

So, the execution of hedging positions goes this way:

“Short 2W (1%) OTM put option, go long in 2 lots of 1M ATM +0.49 delta put options, thereby net delta should remain at around -0.66.”

We used narrowed expiries so as to suit the OTC market trends and to reduce the hedging cost. The quantum in above mentioned strategy is just for demonstration purpose only, one can load up weights according to the FX exposure in their portfolio.