J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill

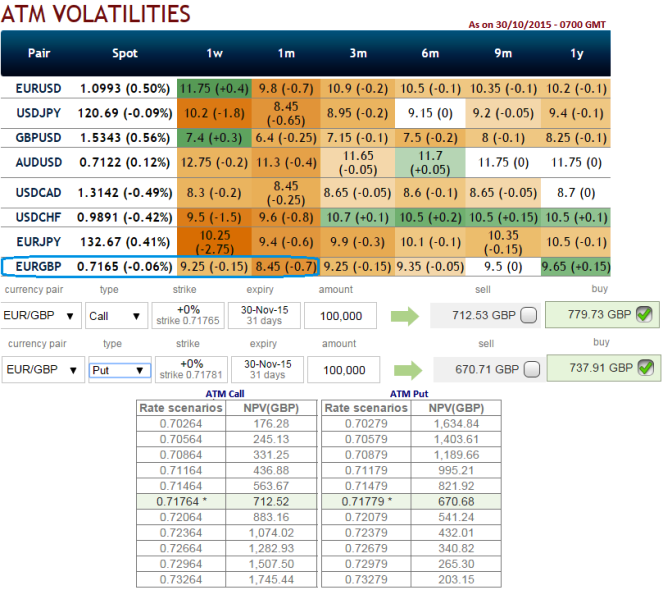

The implied volatility of ATM contracts is at 9.25% and it is expected to reduce at around 8.5% for near month expiries of this the pair.

NPV of 1m ATM call is at 712.52 while the Premiums trading above 9.40% at GBP 779.73 for lot size 100,000 units.

NPV of ATM put is at 670.68 while Premiums trading above 10.02% at GBP 737.91 for lot size 100,000 units.

Thereby, comparing this difference in options premiums and NPV with implied volatility in market sentiments we think the hedging cost would not be economical on downside deploying ATM put instruments.

But we cannot afford to get stuck in this riddle without hedging, so what's the alternative, in forwards markets at least..?

Subsequently, here comes the strategy arbitrage strategy in which options trading that can be performed for a riskless profit as EURGBP ATM call options are overpriced relative to the underlying exchange rate of EURGBP.

To perform this conversion, the hedger holds the underlying spot FX and offset it with an equivalent synthetic short spot FX (long put + short call) position.

Profit is locked in immediately when the conversion is done, the profit would be strike price of call/put - purchase price of underlying + call premium - put premium.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: EUR/GBP ATM puts seem costlier, option arbitration in lieu of shorts on reducing IV

Friday, October 30, 2015 1:30 PM UTC

Editor's Picks

- Market Data

Most Popular