China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different

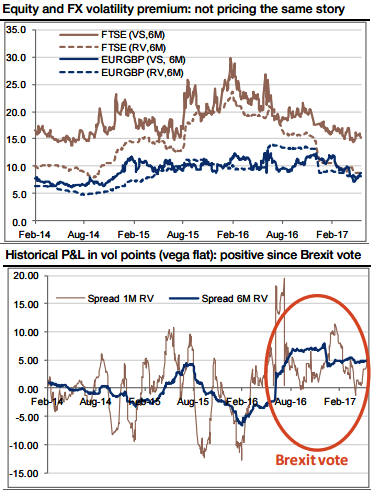

In the UK, we continue to see the Brexit negotiations posing more event risk for markets than the general election result. So, it is worthwhile to keep a track of volatility surface of EURGBP and equity markets of the geography.

The volatility relative value via variance swaps: The 6m variance swap spread between FTSE and EURGBP is currently at 6.3 vol points, but the spread of realized volatilities – the carry – is at 0.7 for the 6m and even slightly negative for the 1m at -0.6 vol points.

We combine the large carry ‘paid’ by the short FTSE variance swap leg to finance the low cost of carrying the EURGBP variance swap leg.

We suggest buying 1.7 times units of EURGBP variance for 1 time unit of short FTSE to achieve a vega-flat structure at inception. We think this is the safe approach, as we see little risk for EURGBP volatility to fall much lower, given that it is at a 2y low and we want to be sufficiently hedged in case of an unexpected surge in FTSE volatility.

Trade mechanism: FX/equity spread of variance swaps, short FTSE Dec-17 variance swap at 15.4, 1 time vega Long EURGBP Dec-17 variance swap at 9.1, 1.7 times vega (GBP notional) Flat spread (indicative bid).

Rationale: The major rationale for this trade has been that the expectations of Brexit to lift EURGBP vol more than FTSE vol.

Risk profile: Equity vol surging more than FX vol Investors going long (short) volatility swap receive the realized volatility above (below) the traded level. However, they must pay the difference between the traded level and realized vol if the latter is lower (higher) than the former at expiry.

Our structure exposes investors to a sharp rise in the equity index volatility, with the 6m FTSE realized volatility ending 1.7 times above the 6m EURGBP realized volatility.