FxWirePro- Woodies pivot (Major)

FxWirePro- Woodies pivot (Major)  NZDJPY Bears Reload as 92 Resistance Caps Bounce; Sell-on-Rallies Eyed Toward 90

NZDJPY Bears Reload as 92 Resistance Caps Bounce; Sell-on-Rallies Eyed Toward 90  AUDJPY Breaks Key Trendline Support — Bears Eye 110 as Momentum Accelerates

AUDJPY Breaks Key Trendline Support — Bears Eye 110 as Momentum Accelerates  FxWirePro: USD/ZAR remains buoyant, looks to extend gains

FxWirePro: USD/ZAR remains buoyant, looks to extend gains  FxWirePro : GBP/NZD uptrend loses steam, remains on bullish path

FxWirePro : GBP/NZD uptrend loses steam, remains on bullish path  FxWirePro- Woodies pivot (Major)

FxWirePro- Woodies pivot (Major)  FxWirePro:GBP/USD recovers slightly from early decline but bears are not done yet

FxWirePro:GBP/USD recovers slightly from early decline but bears are not done yet  FxWirePro: EUR/AUD bullish outlook with scope to target 1.6550

FxWirePro: EUR/AUD bullish outlook with scope to target 1.6550  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  FxWirePro:NZD/USD rout continues without relief

FxWirePro:NZD/USD rout continues without relief  FxWirePro: GBP/NZD gaining momentum for a move towards 2.3100 level

FxWirePro: GBP/NZD gaining momentum for a move towards 2.3100 level  FxWirePro: USD/CAD uptrend loses steam, remains on bullish path

FxWirePro: USD/CAD uptrend loses steam, remains on bullish path  BTC Slips Below $60K as Institutional Demand Dries Up — Bears Eye $59K Support, Rallies to $63K for Shorts

BTC Slips Below $60K as Institutional Demand Dries Up — Bears Eye $59K Support, Rallies to $63K for Shorts  FxWirePro: USD/CAD hits 14-month high , Scope for further upside

FxWirePro: USD/CAD hits 14-month high , Scope for further upside  FxWirePro: GBP/USD heads deeper into bear territory, 23.6% fibonacci eyed

FxWirePro: GBP/USD heads deeper into bear territory, 23.6% fibonacci eyed  ETH Bounces as Shorts Cover, Yet ETF Bleed Warns $1,850 Resistance Won’t Break

ETH Bounces as Shorts Cover, Yet ETF Bleed Warns $1,850 Resistance Won’t Break  EURJPY Bounce Loses Steam Below 184 — Sell-the-Rally Setup Eyes 183 Target

EURJPY Bounce Loses Steam Below 184 — Sell-the-Rally Setup Eyes 183 Target

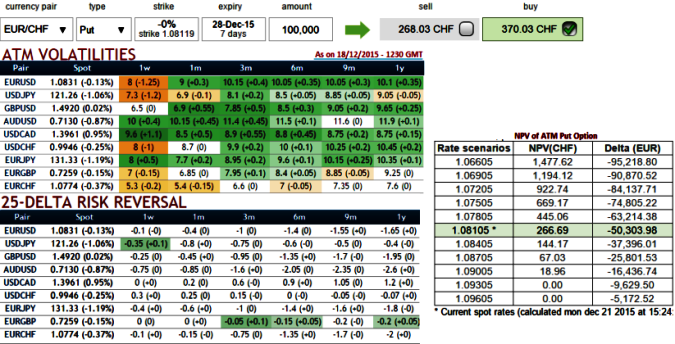

As you can observe the ATM premiums are trading 38% more than NPV, so hedging with these overpriced at the money instruments would not be cost effective as its delta amounting close to 50% would collapse as the time decay implies drastically as the IV is expected to reduce further.

For instance, suppose we've constructed an at the money put option of EURCHF with 1W expiry and with this given maturity has reduced its implied volatility from 6.4% to 5.3% and it is likely to remain in this lackluster zone (historically these vols have never disappointed).

In a true smile, options with an at-the-money strike are priced with a lower volatility than out-of-the-money and in-the-money volatility strikes. Such market occurrences are observable in the EURCHF FX OTC market.

From the nutshell evidencing risk reversals, 25-delta risk of reversals of EUR/CHF the most expensive pair to be hedged for downside risks after AUDUSD as it indicates puts have been overpriced.

As it showed the highest tendency towards downside hedging activity, alternatively synthetic positions would come into arrest these downside risks.

This expensive options situation could be dealt by shorting spot FX and simultaneously by going long in an at the money call.

The payoff function (Profit/Loss) from this strategy replicate exactly as those from the long put positions.

The two combination create a synthetic long ATM put position with the same risk/reward profile of the overpriced ATM put.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: Deploy EUR/CHF synthetic put for hedging as naked puts seem overpriced

Monday, December 21, 2015 10:45 AM UTC

Editor's Picks

- Market Data

Most Popular