Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

As expected by us, China’s investment growth slowed. Latest data showed that China’s fixed asset investment grew 8.6% YoY year-to-date in May, below market expectations and previous reading at 8.9%. After seasonal adjustment, the fixed asset investment gained 0.72% MoM in May, down from 0.75% in April and 0.79% in March.

Clearly, there emerged a gradual downward path in the underlying momentum, indicating that China’s economy will continue to face headwinds in the coming quarters. There are two factors behind the slowing investment momentum.

First, the policy tightening, including the measures in the property and financial sectors, has dragged down the investment. Indeed, the property prices have peaked in China, and the housing sales have illustrated a sluggish momentum in tandem, which somewhat reminds me of the property-led economic slowdown in 2010-2015.

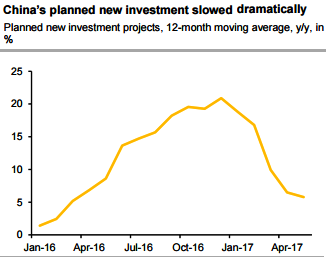

Second, the planned new investment has lost steam entering the year of 2017 (refer above chart), suggesting that the public spending has been gradually fading. Over the full year of 2016, the public stimuli had significantly boosted the investment growth, as suggested by extremely elevated investment from SOEs.

China is a source of angst for global investors with non-financial corporate debt at 166% of GDP compared with 97% a decade ago (refer above chart). The bursting of a debt bubble in China would have far-reaching negative implications for emerging markets either via the risk sentiment channel or through commodity prices, global growth, and the global supply chain.

History tells us that credit booms lead to bubbles and to eventual crises. In China’s case, the risks are compounded by the large size of the banking system relative to GDP (refer above chart). It is unclear if, or when, the bubble will burst in China, but it is the major medium-term risk factor for the entire EM currency complex.

Catalyzed by the PBoC’s announcement of a new CNY fixing formula and the upward squeeze in the CNH interest rates, USDCNY has played catch-up with the broader USD weakness over the past month. As important as these shifts have been in explaining the USDCNY move from 6.90 to 6.80, they remain secondary, in our view, to the fact that China’s underlying BoP position has evolved stronger than market expectations and currency appreciation pressures were already building.