Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules

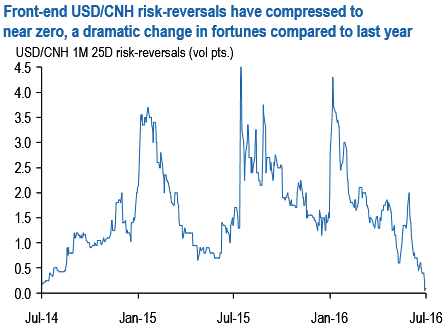

The front-end CNH risk-reversals have shrunk to near zero (see chart) as the PBoC's tight FX management has smashed realized volatility.

CNH vol skews started softening in mid-Q1 when Chinese authorities instituted capital controls to curb capital outflows and have been on a steadily declining trend since alongside a general risk premium compression in China-linked assets.

China risk-reversals in free fall front-end CNH risk-reversals compressed to almost zero this week (see above chart), a rare occurrence in the EM FX world and a dramatic change of fortunes for a currency that was supposed to be spiralling out of control and into a 1990s style crisis only a few months ago.

The move picked up pace this week with 1M 25D riskies falling to 0.05 vols (-0.30 from intra-week highs), effectively signalling symmetric volatility risks in both RMB rallies and sell-offs over the next month.

The optics of nearly flat risk reversals is jarring given the long history of disruptive EM currency weakness that usually commands a healthy premia for USD calls over USD puts, and the more recent macro-narrative of declining growth, unsustainable leverage and capital flight around China that ought to have been priced into options via fatter right tail probabilities (i.e. higher USD call/CNH put prices).

Unsurprisingly, anecdotal accounts indicated investor interest in snapping up zero price CNH riskies purely on price grounds, even if catalysts for a volatile sell-off over the next month are not obvious.

Stay short 6M vol; USD puts/CNH calls are better shorts than ATMs to monetize RMB stasis given the skew set-up.