Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

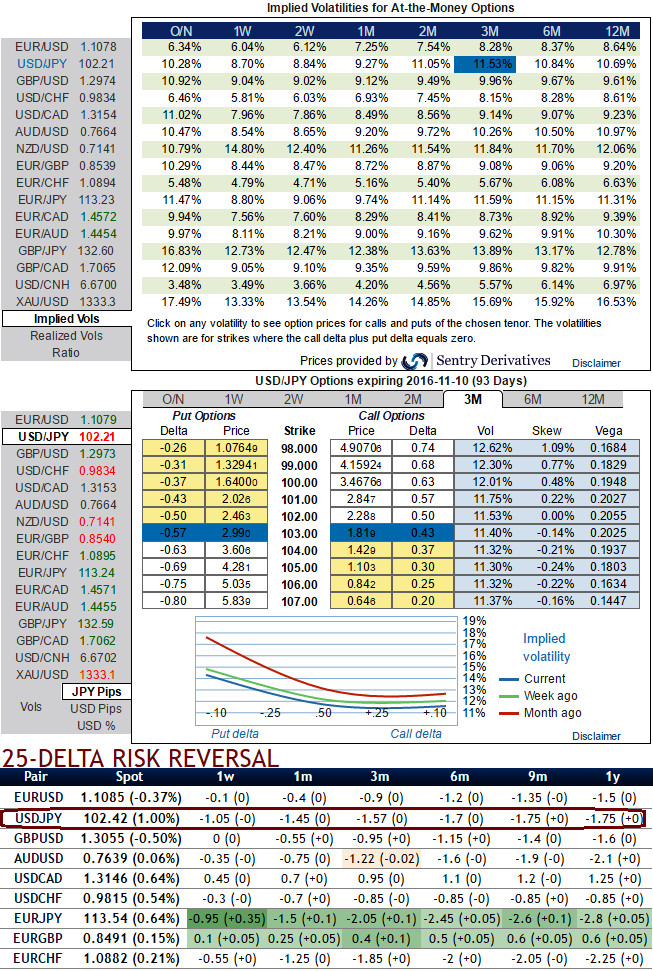

Volatility shocks and the passage of time have opposite effects on the value of a vanilla option (see ATM strikes on USDJPY options). When it can benefit from more volatility (long vega and gamma on OTM put strikes), time has a negative impact every day (short theta).

Yen IVs: Live September meeting should keep 2M vol supported; while yen 1-3m risk-reversals still a better sale as Fed considers global slowdown risks and Brexit settlements which is why the US central bank keeps deferring rate hikes atleast until the end of 2016 or by Q1 of 2017.

Please be noted that the 1m IV skews are more biased towards OTM put strikes, significant changes can indicate a change in market expectations for the future direction in the underlying forex spot rate and these risk reversals evidences the difference in volatility, and therefore price, between puts and calls on the most liquid out-of-the-money (OTM) options quoted on the OTC market.

This loss is the greatest when the spot is close to the option strike, and accelerates as maturity approaches (convergence towards intrinsic value, i.e. the terminal payoff). Conversely, a short volatility strategy gains value with time.

Therefore, long vol directional investors are struggling against the clock while short vol investors are not pressed by the countdown to expiry. The former ‘buy’ market volatility while the latter ‘buy’ time on the market. As a result, long vol directional investors generally are more interested in contemplating an early unwind than short vol investors.