Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis

The RBA and RBNZ appeared to diverge markedly in the recent monetary policy meetings, with the former signaling a near-term pause on easing and messaging steady while the latter surprised with 50 basis points of cuts. Still, we expect both central banks to remain accommodative over the medium-term. The RBA SoMP baked in two cuts in its forecasts, as expected, and even despite that adjustment does not predict meeting its unemployment or inflation objective. Furthermore, Gov. Lowe has reiterated his recent ‘low for long’ expectation and has posited reaching the zero lower bound as a possibility. For now, the RBA retains its easing bias even despite a potential near-term hold.

Meanwhile, the RBNZ has demonstrated its willingness to accommodate aggressively under its new governor, and we expect them to continue their easing cycle later this year in November – especially as bank capital regulation changes begin to set in. Further easing will drive real rates to -1% and should help anchor weakness in both currencies.

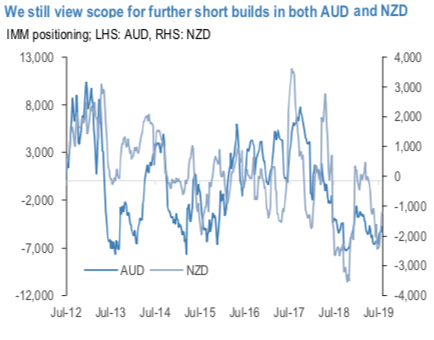

Furthermore, AUD and NZD should both remain under pressure as the US-China trade war creates adverse trade outcomes for other regional partners (refer 1st chart), and continue to force down yields amid higher central bank easing expectations. Neither currency performs well during Fed easing cycles, for example, and both are still prone to the downside so long as global growth indicators continue to slump. A new wrinkle, however, is the sudden depreciation in CNY which has challenged risk sentiment and will likely dent already-slowing demand for imports. And despite the confluence of mostly-negative global developments

along with full-fledged antipodean easing cycles, we don’t view positioning metrics as especially stretched (refer 2nd chart). This should create enough room to let both currencies continue their downward medium-term slide. Near-term drivers to keep an eye on including the ongoing collapse in iron ore prices, AUD data (employment 14-15 Aug and GDP 9 Sept) NZD housing news.

Trade tips:

Stay short NZDUSD in cash. Marked at +0.81%.

Stay short AUDJPY in cash. Marked at +0.67%.

Uphold NZDJPY shorts via 6m put spread. Paid 1.07% at the end of May. Marked at +1.56%. Courtesy: JPM