Citi Raises TSMC Price Target as AI Chip Demand Strengthens Growth Outlook

Citi Raises TSMC Price Target as AI Chip Demand Strengthens Growth Outlook  Goldman Sachs Flags 3 Key Risks Ahead of Europe’s Earnings Season

Goldman Sachs Flags 3 Key Risks Ahead of Europe’s Earnings Season  Vietnam’s population hit the 100 million milestone. Where’s it headed?

Vietnam’s population hit the 100 million milestone. Where’s it headed?  Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’

State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’  Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails

Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails  Smartphones are helping filmmakers tell the stories the movie industry overlooks

Smartphones are helping filmmakers tell the stories the movie industry overlooks  AI can be a personal trainer in your pocket – but is it safe?

AI can be a personal trainer in your pocket – but is it safe?  USA at 250: the Black American struggle for life, liberty and the pursuit of happiness

USA at 250: the Black American struggle for life, liberty and the pursuit of happiness  Trump has made more than $1 billion from crypto in a year. How?

Trump has made more than $1 billion from crypto in a year. How?  Gold Pulls Back After Hitting $4,180 as Geopolitical Risk Sends Crude Higher

Gold Pulls Back After Hitting $4,180 as Geopolitical Risk Sends Crude Higher  Buy the Dip: Gold Holds Strong at $3980, Targets $4150

Buy the Dip: Gold Holds Strong at $3980, Targets $4150

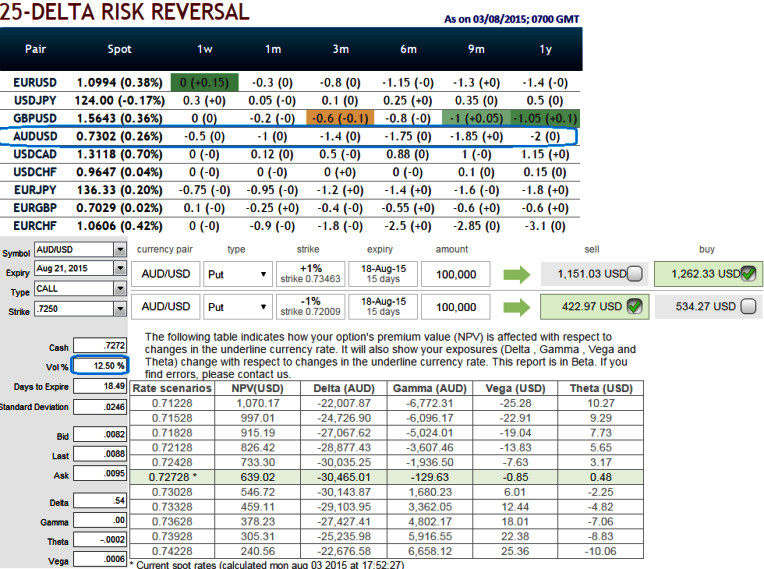

Rationale: Prevailing implied volatility rates for AUD/USD ATM 1M-6M contracts are in range of 12% to 14%. But higher negative delta risk reversal indicates put contracts have been relatively costlier. In the nutshell, AUD/USD Out of the money options are trading with negative delta risk reversal which would mean that downside risk protection is more expensive.

The downside risk in AUD against USD is anticipated as the Fed's rate decision seems to be is in line with the Yellen's hints after she sent strong indications that US economic conditions are likely to justify an interest rate hike at some point this year. But Aussie import prices QoQ are improved by 1.4% which is in line with forecasts.

For Australian exporters who have their receivable exposures in AUD, we advocate gamma spreads rather than naked puts (even OTM puts have been expensive). As the risk appetite varies from different investors to different traders, we've customized our formulation of strategies for such varied circumstances.

When the above naked put option was highly sensitive to the underlying exchange rate of AUD/USD, we think it adds to the risk and reward profile for both options holders and writers. So, buy 15D (1%) In-The-Money 0.15 gamma put option and short 15D (-1%) Out-Of-The-Money put option for net debit.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: AUD/USD delta risk-reversal signifies overpriced puts; HY gamma spreads for IV riddle

Monday, August 3, 2015 12:30 PM UTC

Editor's Picks

- Market Data

Most Popular