Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  Buy the Dip: Gold Holds Strong at $3980, Targets $4150

Buy the Dip: Gold Holds Strong at $3980, Targets $4150  JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026

JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026  Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  Trump has made more than $1 billion from crypto in a year. How?

Trump has made more than $1 billion from crypto in a year. How?  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit

Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

GBP continues to be out of fashion, having weakened 10% on a trade-weighted basis post-Brexit.

BoE meeting Thursday main event. We and consensus look for a 25bps cut, and will look closely at the inflation report to see BoE’s take on Brexit consequences

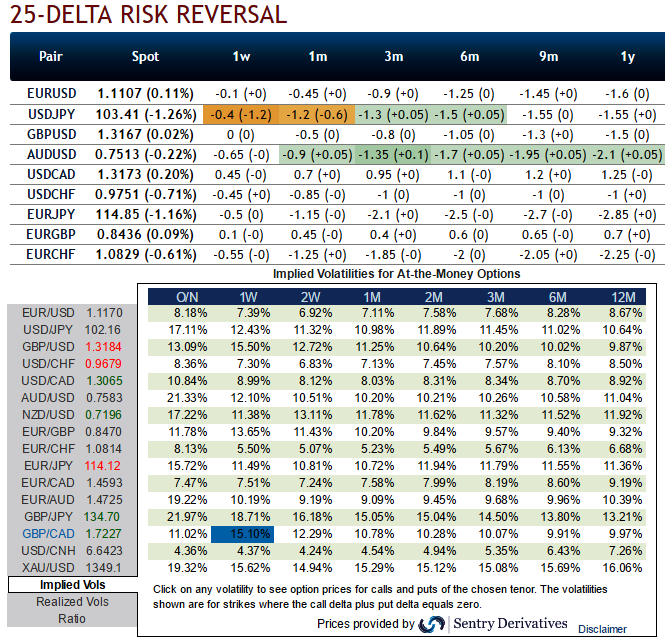

Delta risk reversals of EURGBP: From the nutshell showing delta risk reversals of EURGBP, you can probably make out that the pair has been one of the most expensive pairs to be hedged for upside risks as it indicates calls have been relatively costlier over puts.

As it showed the 2nd highest positive values (after USDCAD) which indicate upside risks of spot FX is anticipated and hedging for such risks is relatively more expensive.

Needless to specify, GBP vols have still been flying with sky rocketed pace no matter what both prior and post Brexit event, but this time these IVs are also owing to BOE’s monetary policy decision.

Post Brexit adjustments saw leveraged funds reduce their net long USD positions for the week ending 28 June. This was despite the DXY rallying following the Brexit result. The USD selling was broad based against all the major currencies.

Whereas on GBP side, further into 2016, there are two key risks associated with sterling – the UK’s unsustainable current account deficit and the post-Brexit formalities promised for end-2017 at the latest.

The OTC options market appeared to be more balanced on the direction for the pair over the 1m to 1y time horizon as hedgers have been cautious on long-term downtrend that has lasted since mid-April 2013 and as a result delta risk reversal for GBPUSD was turning into negative, while the UK current account balance data go back to 1946. The annual deficit (just over £100bn in 2015) didn’t get above £1bn in a single year until 1973, so we reckon the pre-1946 story can be largely ignored. Since 1946, the cumulative deficit is £881bn, and it’s getting bigger and bigger.

This isn’t the only part of the UK balance of payments that is, at first blush, confusing. The net asset position has improved, yet the income on foreign assets has deteriorated. The UK’s net foreign assets are in the hands of a small number of large multi-national companies, many in the resources sector.

The income they earn on overseas investments has fallen because too many are in sectors like energy, where prices have fallen significantly. That worsens the current account balance. But if those weak earnings simply discourage investment in more capacity in these industries, a lower dividend flowing home would be offset by reduced investment overseas in the financial account.

Hence, we think the foreign trade bills in pounds denomination are so needy to be hedged for downside risks and so is evidence in OTC hedging arrangements.