Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

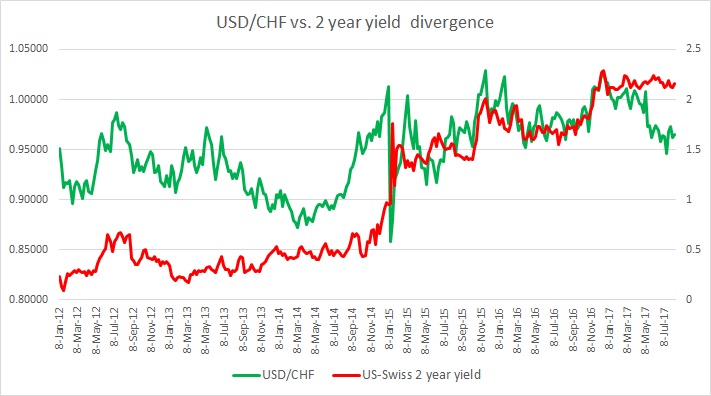

During our evaluation period beginning 2012, the yield spread between the US 2-year bond and a Swiss equivalent has widened by almost 200 basis points but the exchange rate hasn’t followed through as much as it should have been as it benefits from risk aversion inflows. Swiss franc remains the most overvalued currency against the dollar, in terms of yield divergence.

- In recent days, Swiss franc’s correlation with the 2-year yield spread (US-Swiss 2 year) has fallen to negative 16 percent, though, at times, it has shown relatively high positive correlation, as high as 90 percent. Just before and after the Brexit referendum in the UK, the 20-day rolling correlation was averaging above 60. Hence, it is vital to keep a watch on the Swiss yields.

- Just after the Swiss floor shock in January 2015 when the Swiss National Bank (SNB) removed a floor in EUR/CHF at 1.20 this relation went to negative and stayed there until October with an occasional bounce to positive territory. It hasn’t gone much to the negative since, until recently.

- Unlike the euro or the pound, the Swiss franc is considered a safe haven currency; hence the yield relation sometimes gets overlooked. However, Swiss yields are a must watch as they are the lowest for any government bonds in the world and any shift in that will mark a major turnaround in trend.

Since our last review, back in July, there have been minor changes in the spread which is currently at 215 basis points in favor of the dollar. The spread has narrowed by 4 basis points in favor of the Swiss franc since the last review and the franc strengthened by 30 pips and trading at 0.965 per dollar. The 20-day correlation between the exchange rate and yield spread has recovered from negative to positive.

FxWirePro launches Absolute Return Managed Program. For more details, visit http://www.fxwirepro.com/invest